How to compare returns

What you should look out for when comparing your different investments and their returns

Sometimes you have more than one form of investment, for example a pillar 3a, two different investment apps for unrestricted pension provision and fund investments with a bank. In this article, we explain what you should keep in mind when comparing the returns of the different forms of investment.

Time window

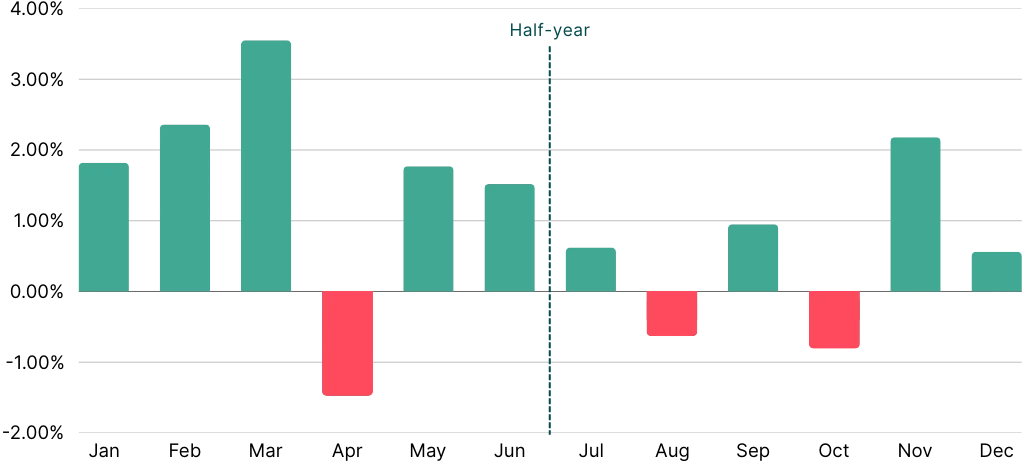

It was particularly noticeable in 2024: the returns were not spread evenly throughout the year, but mainly in the first half of the year. This means that anyone who only made an investment during the summer was unable to benefit from the strong first six months.

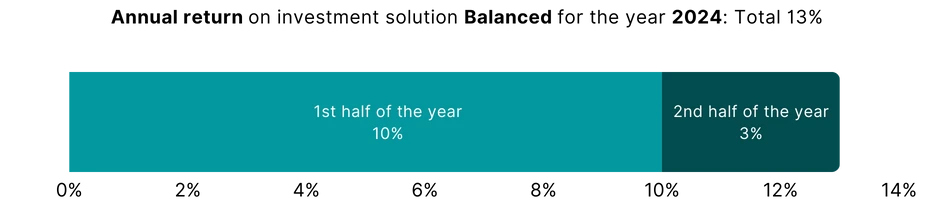

Strong first half-year

The findependent investment solution “Balanced” achieved a total return of 13% in 2024, after deduction of all costs. 10% was generated in the first half of the year and 3% in the second half.

Don’t: Don’t compare an investment that you started on 1 January or in the previous year with an investment started during the year.

Do: Instead, look at the return for the entire calendar year for your investment made during the year. Or shorten the time window for the existing investment to the same length as your new investment.

Investment amount

This aspect is relevant if you are not observing a percentage change (specifically the time-weighted return TWR) for the return comparison, but the actual monetary change. The higher your original investment amount, the higher the return in Swiss francs (positive or negative).

Don’t: Do not use the monetary change for the comparison.

Do: Always use the time-weighted return TRW for return comparisons.

MWR / TWR

findependent calculates the return in the app as a time-weighted return (TWR). Although this type of calculation is considered standard in the financial sector, it can give you the feeling that return and profit do not match.

The reason for this is that all incoming and outgoing payments are ignored when calculating the TWR. This means that the return corresponds to the return that would have been achieved if the same amount had always been invested from the outset. This allows different investment solutions and strategies to be compared fairly.

The major disadvantage of this method of calculation is that the return does not correspond to the intuition (profit or loss divided by the total value of the investment solution) as soon as you have made more than just a single payment into your investment solution.

This is why findependent also shows the money-weighted return (MWR). This takes into account the personal payment dates, which means that the return often corresponds well with the actual profit or loss and is therefore easier to understand.

Deposits and withdrawals

You may have made deposits or withdrawals over the course of the year. These will affect your money-weighted return. For example, if you have made an additional deposit shortly before a sharp rise in the share price, this investment solution will show a higher money-weighted return than an investment solution to which you have not allocated any additional funds.

Don’t: Don’t compare money-weighted returns if you have a different deposit and withdrawal pattern with one investment solution than the other.

Do: Use time-weighted returns to measure and compare the actual performance of the investment.

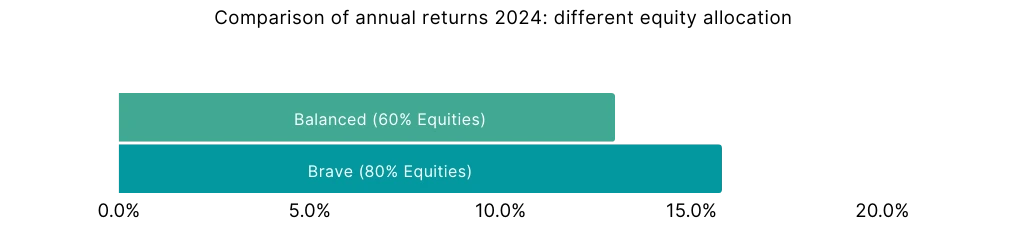

Investment strategy

Different asset classes deliver returns at different levels. This was no different in 2024. While global equities gained 27%, bonds delivered 6% and properties almost 10%. Accordingly, mixed portfolios performed differently, depending on their weight in equities.

It’s true for 2024 and especially for the long term: the more equities in the portfolio, the higher the return (and the higher the fluctuations in value).

Don’t: Don’t compare a pure equity strategy with a mixed portfolio.

Do: Compare a mixed portfolio with, for example, 40% equities with an investment solution with approximately (+/- 5%) the same proportion of equities.

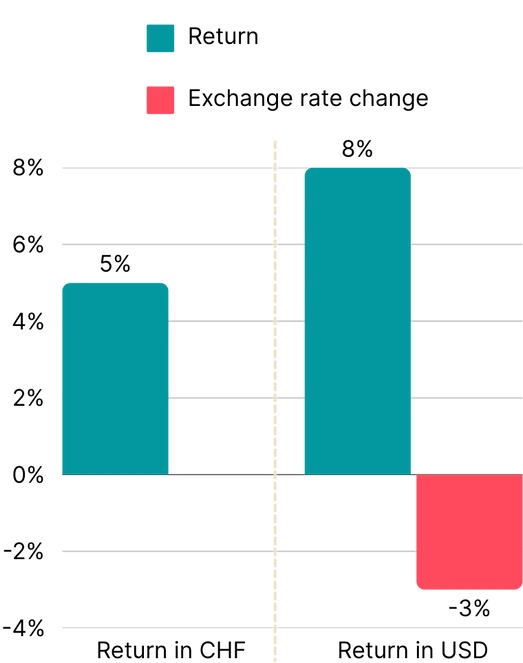

Currency

The Swiss franc is hugely important to us; we pay practically all our obligations in this country in our national currency. The situation is somewhat different in a global context, where the Swiss franc plays a rather subordinate role. Many global investments are calculated in US dollars. If you make such investments, there is an exchange rate risk. A return in a foreign currency must be adjusted for the change in the exchange rate in order to obtain a return in Swiss francs.

Don’t: Don’t: Do not directly compare returns on an investment in a foreign currency with returns on an investment in Swiss francs.

Do: Always adjust returns on an investment in a foreign currency for the change in the exchange rate against the Swiss franc in order to be able to compare with an investment in CHF.

Actual returns

You may rely on a generic information sheet for your fund investment to compare returns. The returns may not be listed in the same currency and not net (after deduction of all costs). The main currency of the fund may be euros, but your actual investment is denominated in Swiss francs.

If this is the case, the returns of these two currency tranches are not the same, and sometimes the returns are shown before costs are deducted. This is usually due to the fact that there are many different variants of the same “main investment” and each variant has a different cost structure.

Don’t: Don’t simply take the returns from a marketing document from your bank and compare them with the returns achieved with another investment solution.

Do: Always use actual returns. In other words, what was actually achieved in terms of asset growth, in Swiss francs and after deduction of all costs.

Conclusion

Comparing returns makes sense. After all, at the end of the day, it is only the net returns that count. Nevertheless, apples should not be compared with pears. The time of deposit and the chosen investment strategy play a decisive role, especially when looking at a rather short period of time, for example one year. It is therefore advisable to only compare identical time frames and risk profiles and always pay attention to the currency.

This might also interest you

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_for_the_half_savvy_june_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 16:03:422026-06-09 13:03:55Webinar:

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_for_the_half_savvy_june_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 16:03:422026-06-09 13:03:55Webinar:Investing for the (half) savvy (in German)

June 8, 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_for_children_aug_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 15:56:172026-05-06 15:56:17Webinar:

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_for_children_aug_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 15:56:172026-05-06 15:56:17Webinar:Investing for children (in German)

August 24, 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_in_a_nutshell_sep_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 15:39:152026-05-06 15:47:26Webinar:

https://stage.findependent.ch/wp-content/uploads/2026/05/findependent_webinar_investing_in_a_nutshell_sep_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-05-06 15:39:152026-05-06 15:47:26Webinar:Investing in a Nutshell

September 28 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2026/03/findependent_webinar_move_to_the_securities_firm_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-03-24 18:01:492026-04-16 10:17:25Webinar:

https://stage.findependent.ch/wp-content/uploads/2026/03/findependent_webinar_move_to_the_securities_firm_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2026-03-24 18:01:492026-04-16 10:17:25Webinar:Move to securities firm

April 15, 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_children_dec25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-26 16:45:412025-12-02 10:49:04Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_children_dec25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-26 16:45:412025-12-02 10:49:04Webinar:Investing for children (in German)

December 01, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/11/findependent_webinar_investing_in_a_nutshell_january_12_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-25 10:48:442026-01-13 14:03:13Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/11/findependent_webinar_investing_in_a_nutshell_january_12_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-25 10:48:442026-01-13 14:03:13Webinar:Investing in a Nutshell (in German)

January 12, 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2025/11/findependent_webinar_investing_for_the_half_savvy_february_23_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-04 11:15:032026-02-24 11:47:33Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/11/findependent_webinar_investing_for_the_half_savvy_february_23_26_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-06-04 11:15:032026-02-24 11:47:33Webinar:Investing for the (half) savvy (in German)

February 23, 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2026/02/findependent_webinar_investing_in_a_nutshell_04_05_26_vorschaue.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-02-23 16:15:332026-05-05 09:34:42Webinar:

https://stage.findependent.ch/wp-content/uploads/2026/02/findependent_webinar_investing_in_a_nutshell_04_05_26_vorschaue.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2025-02-23 16:15:332026-05-05 09:34:42Webinar:Investing in a Nutshell

May 04 2026

7pm

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2024/08/findependent_webinar_anlegen_fuer_kinder_vorschau_18-11_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-10-31 10:00:332024-12-02 11:37:39Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/08/findependent_webinar_anlegen_fuer_kinder_vorschau_18-11_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-10-31 10:00:332024-12-02 11:37:39Webinar:Investing for children (in German)

November 18, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2024/10/findependent_webinar_anlegen_einfach_erklaert_qoqa_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-10-01 15:23:472024-11-25 12:19:17QoQa x findependent Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/10/findependent_webinar_anlegen_einfach_erklaert_qoqa_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-10-01 15:23:472024-11-25 12:19:17QoQa x findependent Webinar:Investing in a Nutshell

October 9, 2024

12:30 pm

https://stage.findependent.ch/wp-content/uploads/2024/10/findependent_webinar_investing_in_a_nutshell_february_17_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-09-30 23:54:432025-02-18 01:36:47Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/10/findependent_webinar_investing_in_a_nutshell_february_17_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-09-30 23:54:432025-02-18 01:36:47Webinar:Investing in a Nutshell (in German)

February 17, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_webinar_investing_in_a_nutshell_march_25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-31 12:14:032025-03-25 14:53:49Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_webinar_investing_in_a_nutshell_march_25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-31 12:14:032025-03-25 14:53:49Webinar:Investing in a Nutshell (in English)

March, 24 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_webinar_anlegen_fuer_halbprofis_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-26 15:14:412024-11-25 12:19:17Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_webinar_anlegen_fuer_halbprofis_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-26 15:14:412024-11-25 12:19:17Webinar:Investing for the (half) savvy (in German)

September 9, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2024/08/findependent_webinar_anlegen_einfach_erklaert_14_10_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-26 14:50:272024-11-25 12:19:17Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/08/findependent_webinar_anlegen_einfach_erklaert_14_10_vorschau_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-26 14:50:272024-11-25 12:19:17Webinar:Investing in a Nutshell (in German)

October 14, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://stage.findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed?

https://stage.findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed? https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal https://stage.findependent.ch/wp-content/uploads/2024/06/findependent_crowdinvesting_webinar_25_06_vorschau_update.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-06-06 09:26:262024-11-25 12:19:17findependent Crowdinvesting Webinar

https://stage.findependent.ch/wp-content/uploads/2024/06/findependent_crowdinvesting_webinar_25_06_vorschau_update.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-06-06 09:26:262024-11-25 12:19:17findependent Crowdinvesting WebinarJune 25, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_qoqa_webinar_investing_in_a_nutshell_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-05-01 14:37:092024-11-25 12:19:17QoQa x findependent Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_qoqa_webinar_investing_in_a_nutshell_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-05-01 14:37:092024-11-25 12:19:17QoQa x findependent Webinar:Investing in a Nutshell (in German)

May 8, 2024

12:30 pm

https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works

https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2024/03/findependent_webinar_investing-in-a-nutshell_may24_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-03-19 16:28:392024-11-25 12:21:42Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/03/findependent_webinar_investing-in-a-nutshell_may24_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-03-19 16:28:392024-11-25 12:21:42Webinar:Inesting in a Nutshell (in German)

May 13, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This

https://stage.findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors

https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors https://stage.findependent.ch/wp-content/uploads/2024/02/findependent_ladies_event_with_missfinance_may_22_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-02-21 22:04:532025-05-23 10:58:17Registration closed

https://stage.findependent.ch/wp-content/uploads/2024/02/findependent_ladies_event_with_missfinance_may_22_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-02-21 22:04:532025-05-23 10:58:17Registration closed findependent Ladies’ Event in Zurich

May 22, 2025

6 PM

in German

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_for_the_half_savvy_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-02-20 21:42:462025-05-27 09:56:33Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_for_the_half_savvy_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-02-20 21:42:462025-05-27 09:56:33Webinar:Investing for the (half) savvy (in German)

May 26, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_in_a_nutshell_vorschaue.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-24 22:19:242025-06-12 10:13:16Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_in_a_nutshell_vorschaue.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-24 22:19:242025-06-12 10:13:16Webinar:Inesting in a Nutshell (in German)

June 11, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_with_a_plan_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-01 15:16:232025-07-03 13:20:11Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_webinar_investing_with_a_plan_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-01 15:16:232025-07-03 13:20:11Webinar:Investing with a plan: here’s how (in German)

July 02, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_event_crowdinvesting_zh_2024_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-01 11:10:442024-06-28 10:46:32findependent Crowdinvesting Event in Zurich (in German)

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_event_crowdinvesting_zh_2024_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-01-01 11:10:442024-06-28 10:46:32findependent Crowdinvesting Event in Zurich (in German) 26. June 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_children_aug25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-30 17:28:122025-08-05 14:15:17Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_children_aug25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-30 17:28:122025-08-05 14:15:17Webinar:Investing for Children (in German)

August 04 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_the_half_savvy_sep25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-29 19:32:402025-09-11 09:44:45Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_for_the_half_savvy_sep25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-29 19:32:402025-09-11 09:44:45Webinar:Investing for the (half) savvy (in German)

September 10, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_in_a_nutshell_oct25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-28 16:46:052025-10-07 10:36:51Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_in_a_nutshell_oct25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-28 16:46:052025-10-07 10:36:51Webinar:Investing in a Nutshell (in German)

October 06, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_get_together_29_oct_25_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-27 17:45:442025-09-17 13:00:58findependent Get Together in Zurich

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_get_together_29_oct_25_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-27 17:45:442025-09-17 13:00:58findependent Get Together in Zurich October 29, 2025

7 pm (in German)

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_with_a_plan_nov25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-27 16:52:052025-11-04 17:45:00Webinar:

https://stage.findependent.ch/wp-content/uploads/2025/06/findependent_webinar_investing_with_a_plan_nov25_preview.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-27 16:52:052025-11-04 17:45:00Webinar:Investing with a plan (in German)

November 03, 2025

7pm

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_event_crowdinvesting_aarau_2024_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-06 14:47:382024-06-28 10:47:04findependent Crowdinvesting Event in Aarau (in German)

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_event_crowdinvesting_aarau_2024_preview_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-12-06 14:47:382024-06-28 10:47:04findependent Crowdinvesting Event in Aarau (in German) 27. June 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_Webinar_Investing_in_a_Nutshell_November_22_23_Vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-10-19 13:55:552024-11-25 12:21:42Webinar:

https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_Webinar_Investing_in_a_Nutshell_November_22_23_Vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-10-19 13:55:552024-11-25 12:21:42Webinar:Investing in a Nutshell

November 22, 2023

7 PM

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_webinar_anlegen_einfach_erklaert_vorschaue_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-05-28 23:30:492024-11-25 12:21:42Webinar:

https://stage.findependent.ch/wp-content/uploads/2024/05/findependent_webinar_anlegen_einfach_erklaert_vorschaue_en.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2023-05-28 23:30:492024-11-25 12:21:42Webinar:Inesting in a Nutshell (in German)

August 6, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland

https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple!

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple! https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland https://stage.findependent.ch/wp-content/uploads/2022/08/findependent_webinar_investing_for_the_half_savvy_may24_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2022-08-16 16:36:552024-11-25 12:22:32Webinar:

https://stage.findependent.ch/wp-content/uploads/2022/08/findependent_webinar_investing_for_the_half_savvy_may24_vorschau.webp

810

1080

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2022-08-16 16:36:552024-11-25 12:22:32Webinar:Investing for the (half) savvy (in German)

May 22, 2024

7pm

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent