Smart deposit and investment behaviour

This is the best way to invest your money

You’ve finally decided to start investing, but you’re still unsure about how exactly to go about it? In this blog post, we will go into the most important points about deposit strategies and investment behaviour. We answer questions like: What is the best investment strategy? What is the smartest way to invest and what does a logical deposit strategy look like?

Let’s assume that you have decided to invest around 10’000 Swiss francs. You do not want to touch the money for the next 10 years. Now you ask yourself when and at what intervals you should invest it. Annually, monthly or quarterly? Do you prefer to invest at the beginning of the month or at the end of the month? Should you invest it all at once or in tranches?

First of all, we would like to point out that the deposit strategy strongly depends on your personal financial situation. We have even dedicated a separate blog post to the question of whether to invest everything at once or gradually. You can read it here.

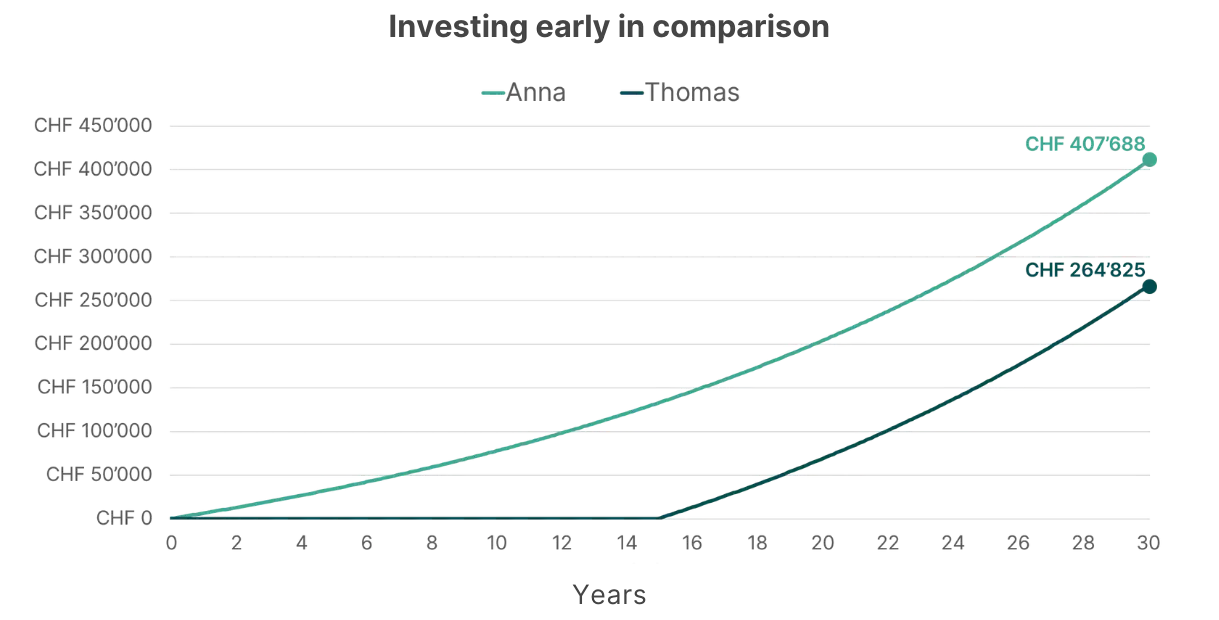

Basically, the earlier you invest, the more you benefit from the compound interest effect.

Calculate your personal compound interest effect with our compound interest calculator.

Compound interest effect

Compound interest is interest that accrues not only on the money invested but also on the interest already earned from the previous year. It helps to increase the performance of your investments. The longer you keep your money invested, the more the compound interest effect comes into play. Another side note: By interest, we mean the return, i.e. the increase in the value of your investment. You could also call the “compound interest” “return returns”.

If you are unsure, we recommend that you start with regular smaller amounts and then increase them over time. Especially if you are new to this topic, you may be a little unsettled at the beginning when you see your investments fluctuate, although this is quite normal.

At findependent, you invest the first 2’000 Swiss francs without management and custody fees for life. So if you are still unsure, you can try out findependent for free.

With a gradual investment you reduce the risk of catching a “bad” moment. The intervals at which a deposit should be made are not an exact science. The easiest thing to do is to set up a monthly standing order in your e-banking, so you don’t always have to remember to do it. This is also how the majority of findependent investors do it.

How do I know what is the best time to invest my money?

Speculating on the right time usually does not work. Likewise, it is not correct to predict tomorrow’s economic events based on the current situation. We have already gone into these points in detail above. None of us knows how the markets will behave. That is why we at findependent do not make “market forecasts”, which you should always take with a grain of salt anyway.

An old stock market saying goes: “Time in the market beats timing the market”. Various studies have proven this statement. Investors who remain invested in a broadly diversified portfolio over the long term usually achieve a higher return than those who try to stay one step ahead of market developments through targeted purchases and sales.

To the question of what is the best time to invest, we answer with: Now! Now is the best time to invest your money.

The chart below illustrates the importance of starting to invest as early as possible. Anna and Thomas both invested the same amount of money every month. However, after 30 years Anna has almost twice as much fortune as Thomas. Even if you start “only” 15 years later, it can cost you half of the potential fortune. This example should illustrate the importance of early investment timing.

How do I set up a concrete savings plan?

Before you finally decide to invest your money, we would like to give you a few important points to consider. You should answer the following questions for yourself:

- What type of investor am I? Do I like to take risks or do I want to play it safe?

- Can I cope with short-term price declines?

- How long is my investment horizon? 2 or 20 years?

- When do I need my saved fortune again?

- What is my savings goal? Do I want to invest the money until retirement? Am I planning to buy a house?

If you decide to join findependent, you will fill in a questionnaire during registration, which will help you to determine your investment strategy. This questionnaire will cover the above questions, among others.

Once you know which investment strategy you want to pursue and you know how much money you want to invest, you can start.

So far there are no (low-cost) ETF savings plans in Switzerland. However, you can easily create an ETF savings plan yourself by regularly investing money in an ETF investment solution.

If you want to know which ETFs findependent uses for its investment solutions, then you can look it up here.

At findependent there is no fixed term. You can sell and exit your investments at any time (without termination fees). You can also determine the deposit rhythm and the amount of the savings amounts individually. In this way, you can create the ETF savings plan that suits you.

What should I do in case of losses?

The answer to this question is quite simple: Do nothing!

Doing nothing and sitting out crises is the best strategy. Price fluctuations are quite normal and are part of investing. Since securities are traded on the stock exchange, prices also fluctuate constantly. But this is normal and should not bother you. Temporary losses of 30%-50% (in extreme situations) may not feel good, but they are part of investing and should not upset you. So far, the global economy and the Swiss financial market have recovered from every crisis.

If you need further input, we recommend our blog post Behaviour in times of crisis.

A few final tips and tricks

Finally, here are a few last tips that will make you a stock market pro:

- Set your strategy at the beginning and stay true to your goal

- Think long-term and leave emotions out of it

- Invest your money regularly and try to resist the urge to sell when prices fall.

- Stay calm and don’t let stock market news drive you crazy

- When changing life situations (birth of a child, new job, etc.) it is worth adjusting the investment strategy.

- Arrange a free consultation with findependent and let us advise you personally.

You might also be interested in

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent