Investing pension fund money

Step by step to success

When you retire, you have the option to withdraw your pension fund as a lump sum. Investing this money wisely can make a big difference in your financial security during retirement. But where do you start? Our step-by-step guide will help you invest your pension fund easily, transparently, and cost-effectively—so you can enjoy a worry-free retirement.

5 steps to successfully investing your pension fund money

If you choose to withdraw your pension fund as a lump sum and invest it, a structured approach can help. This way, you’ll find the right balance between liquidity needs, risk tolerance, and life expectancy.

Step 1 – Get an overview

Start with a simple budget plan:

- List your income (e.g., social security, rental income, side earnings).

- Compare it with your expenses, including one-time costs like car repairs or travel.

- Factor in larger expenses in the early retirement years (e.g., home renovations, early inheritance gifts, etc.).

Struggling with step 1?

No worries! Schedule a free and non-binding conversation with Kay. He is the co-founder of findependent, has nearly 30 years of experience in the financial industry, and is a financial planner, analyst, and wealth manager.

Step 2 – Set clear goals

This step isn’t easy, but it’s essential. Define your expectations for your pension fund money by answering the following questions:

- What return do you find attractive?

Here are some benchmarks: Savings accounts yield around 0.5%. The average inflation rate for 2024, according to the Federal Statistical Office, is 1.1%. A stock portfolio typically generates around 6% annual returns (after costs).

- Do you want to live off the returns?

Some prefer not to touch their capital and live solely off the returns. Maybe your main goal is to pass on as much of your pension fund money as possible to your heirs.

- Are you planning a gradual capital drawdown?

If you know you’ll need to withdraw from your pension fund over time, this insight will help you set the right strategy and choose the best investment solution.

- How frequently do you want to receive returns?

Would you prefer monthly payouts, or would quarterly or annual distributions work for you?

Step 3 – Assess your knowledge and interest

Reflect on your past experience with investments. How did market fluctuations affect you? Evaluate your own financial knowledge. Also, ask yourself how interested you are in managing investments – do you want to be actively involved in the long run, or would you rather delegate the management of your pension fund money?

When you start with findependent, all the important points are clarified in a brief questionnaire so that you can find the right investment solution for you. Ready-made investment solutions from CHF 500, personalized investment solutions from CHF 5’000.

Step 4 – Create a wealth plan

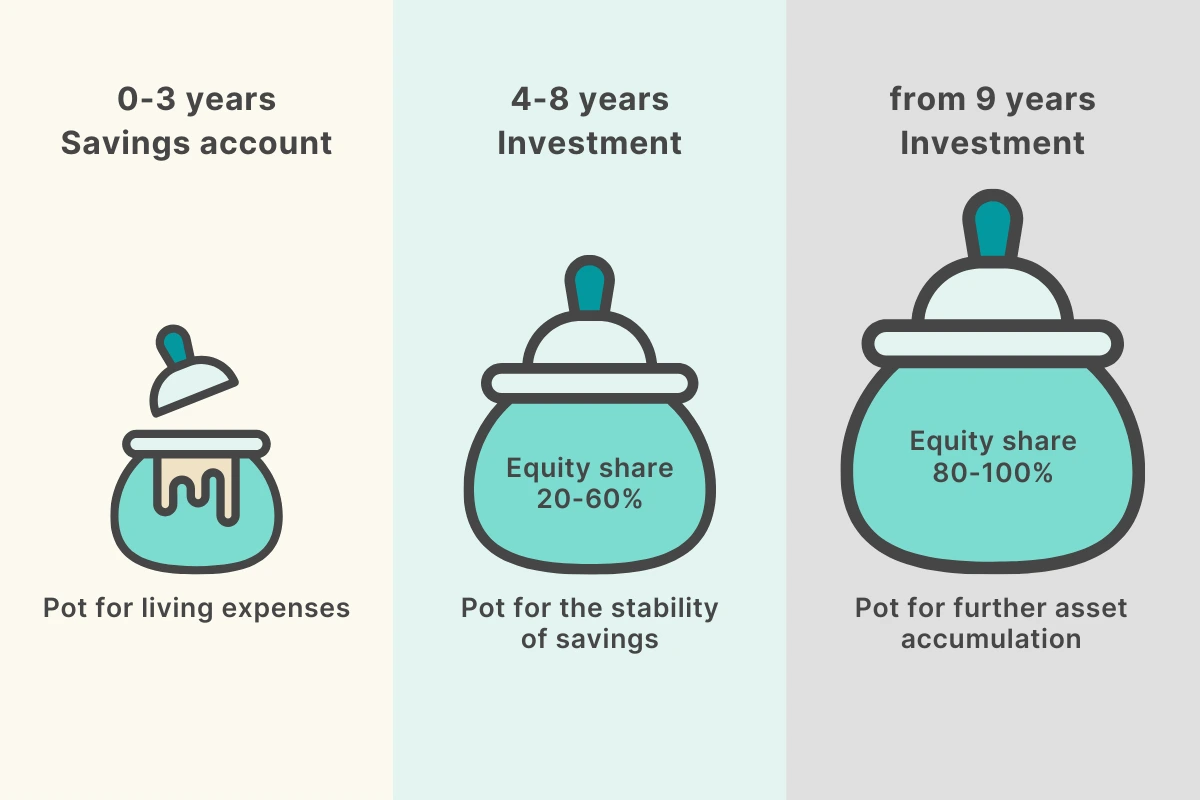

Divide your capital into different “buckets”:

- Bucket A) Liquidity for 0-3 years → Keep in cash, do not invest.

- Bucket B) Medium-term, 4-8 years → Invest with 20-60% in stocks.

- Bucket C) Long-term, 9+ years → Invest with 80-100% in stocks.

To determine the right investment solutions for buckets B and C, go through our questionnaire in the findependent app. Important: Answer the questions with each specific bucket in mind, not your overall wealth.

This is findependent

Founded by Matthias Bryner, the fintech startup findependent has developed a simple, easy-to-understand, and cost-effective investment app. findependent AG is a FINMA-licensed asset manager, and its team currently consists of ten employees. Investor Roland Brack joined through the TV show “Die Höhle der Löwen.” Since its market launch in February 2021, findependent has gained over 25,000 customers, 1,500 of whom are also co-owners through the successful crowdinvesting campaign in summer 2024.

A concrete example with numbers: Your pension fund balance is 400,000 CHF

A) This bucket should contain 60,000 CHF. In Step 1, you determined that, in addition to your OASI income, you will need around 20,000 CHF annually to cover your expenses.

B) This bucket should contain 100,000 CHF. The 20,000 CHF mentioned in A) will also be needed in the medium term. You have no additional planned expenses.

C) This bucket will contain the remaining 240,000 CHF.

A) This bucket will be emptied within around 3 years. After that, you can refill it with money from Bucket B. You can either do this directly with the amount for the next 3 years or on an annual basis.

B) You’ve invested Bucket B with a defensive-moderate investment solution. The 100,000 CHF will remain stable and serve to refill Bucket A after three or six years.

C) The 240,000 CHF in Bucket C have been invested for the long term. After 8-10 years, this bucket will have grown to around 400,000 CHF.

It makes sense to review this division and your liquidity needs every few years and adjust if necessary.

In words instead of numbers: If you let a portion of your pension fund money work for you long-term and effectively, your wealth can remain fairly stable even with annual withdrawals.

Step 5 – Find providers & solutions

To implement your wealth plan, you need a reliable partner. When searching for the right provider, you should consider the following points:

Products / Instruments

The most suitable instruments are ETFs(exchange-traded funds). ETFs are both very cost-effective and allow you to make a well-diversified investment—two key success factors in investing.

Of course, you can choose your own ETFs. Almost 2,000 different ETFs are traded on the Swiss SIX exchange. That can quickly become like searching for a needle in a haystack. Alternatively, you can choose the ready-made investment solutions from findependent, just like 25,000 other customers. Our investment committee has selected and combined the ETFs based on strict selection criteria, regularly reviewing them and making adjustments when necessary.

Flexibility

Look for a provider that allows you to run multiple investment goals simultaneously. This way, you can have a complete overview of your investments with just one app. Usually, the liquidity buffer is kept in a traditional bank account and is not part of this overview.

You can, of course, place the above-mentioned buckets for medium- and long-term investments with different providers. There’s little against this, as long as you maintain an overview and don’t pay unnecessary fees.

It’s also important that you can make simple and quick adjustments to your investment solutions. These adjustments should be possible without additional transaction fees.

The regular payouts must also be easy to process.

The final point concerns contract flexibility. You should only choose providers that do not require a minimum term, meaning you should be able to cancel at any time.

Reputation and security

Make sure to choose an asset manager that is regulated by the Swiss Financial Market Supervisory Authority (FINMA). FINMA ensures strict oversight and adherence to financial regulations.

Your asset manager works with a bank or is itself a custodian bank—make sure that they are connected to esisuisse, which guarantees deposit protection up to 100,000 CHF per customer. The 100,000 CHF that are secured cover the account balance or liquidity of your investment solution. Money invested in (physically replicated) ETFs is considered special assets and will not be part of the bankruptcy estate in case of insolvency. Your investments legally belong only to you.

Access is often provided through an app. It is important that all transactions are secured with the latest encryption technologies and that two-factor authentication is offered as an additional security layer by default. The provider should also regularly undergo independent security audits.

Look for simple, transparent, and regular reporting—you should always have full insight into the investments made, the current portfolio, and the resulting returns.

Service and advice

When choosing an app for your investment solution, look for an intuitive, clear design where all functions are easily accessible. Despite all the technical tools, it’s still wise to have direct access to the team when needed. This access can be through phone, email, or even a personal conversation. A quick, helpful support system and communication on equal terms are crucial elements for building additional trust.

Often, online reviews can give you an impression of the quality and scope of service and advice.

If your digital asset manager regularly offers free webinars, you also have the opportunity to delve deeper into the topic of investments when needed, though it’s an option, not a requirement.

Costs and Fees

Be sure to compare the costs and fees of different providers. The costs are made up of management and custody fees, product costs, and one-time fees.

According to the online comparison service moneyland, a traditional asset management mandate from a bank costs 1.37% annually in management and custody fees. A more affordable alternative is the offer from findependent, with 0.29% to 0.40% per year, depending on the investment amount — the more you invest, the lower the fees.

Product costs are the costs incurred for the instruments used. Expensive instruments include strategy funds and actively managed funds (1.5% to 2.5% or more). Cheap alternatives are ETFs. A balanced portfolio of different ETFs and asset classes should typically cost around 0.1% to 0.25%.

Make sure there are no minimum fees and that you are not charged transaction fees. In general, deposits and withdrawals should be free, and there should be no cancellation fees.

In this context, a key question is whether you want to manage and monitor your investments yourself, or if you prefer to delegate the entire task to an asset manager. A detailed discussion on this topic can be found here.

Tax aspects

The return on an investment solution consists of earnings and capital appreciation. Specifically: With an assumed total return of 5%, around 3.5% comes from capital appreciation and is thus tax-free capital gain. About 1.5% therefore represents taxable earnings. These must be reported in the tax return under wealth income.

To save you time, you should ensure that your provider automatically and free of charge creates an e-tax statement for you. You can then upload it as a PDF file into the electronic tax return (drag-and-drop), and all wealth and income tax values will be transferred in seconds.

Some providers charge extra for this tax statement, CHF 100 or more. With findependent, the e-tax statement is free. For more details on the taxation of findependent investment solutions, check out our blog article.

Common mistakes and how to avoid them

Error 1: Playing it too safe

Since it’s retirement savings, it’s understandable that you’d want to protect yourself from potential losses and might lean toward safer investment options—or even avoid investing altogether. But if you simply leave your pension fund money in a bank account or in poorly yielding fixed deposits, you risk losing it to inflation. We’ve written a detailed article about this.

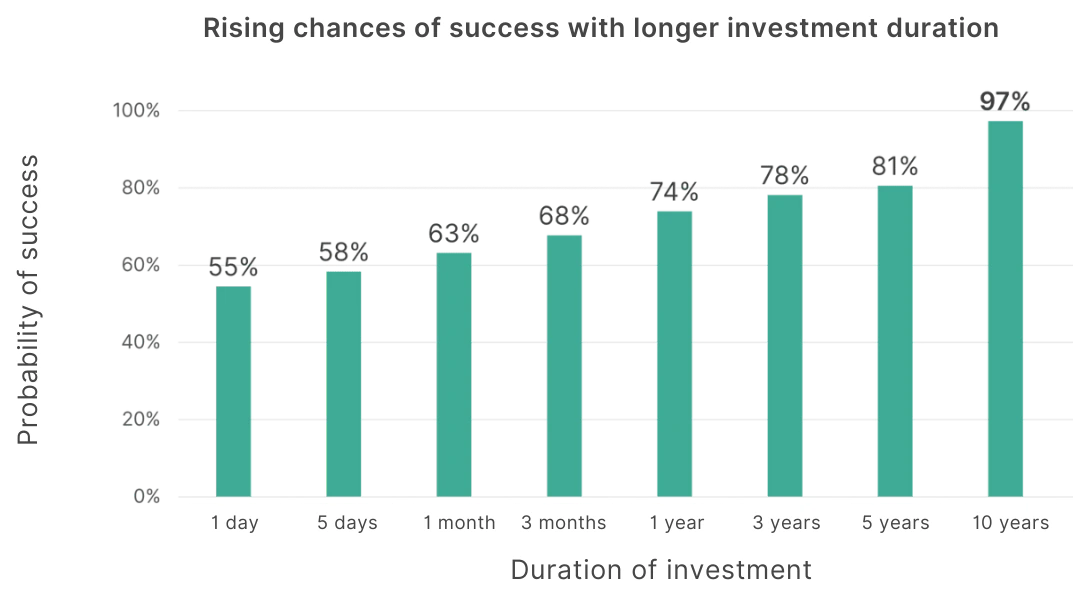

By investing, you can grow your retirement savings over time and protect yourself from inflation. Remember, time and patience are two of the most important factors when it comes to investing.

The risk of making a loss decreases significantly over time with a well-diversified investment solution.

Mistake 2: Only one investment strategy

In most cases, you don’t need immediate and full access to all your pension fund money. Therefore, divide the assets based on time horizons and choose individual investment strategies. For the portion that should be available in the medium term, a more conservative investment strategy is recommended. For the medium to long-term portion, you can choose an equity allocation of 60% or even more.

Mistake 3: Choosing too expensive products and providers

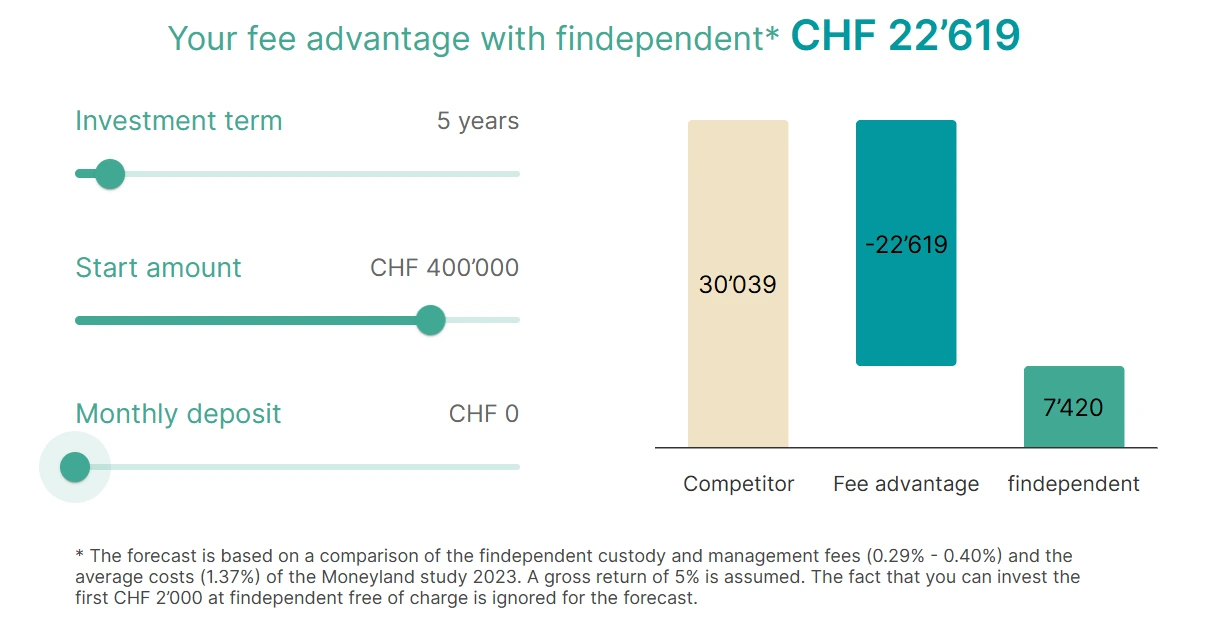

Even seemingly small percentage fees make a significant difference. With an affordable provider like findependent, you can save thousands of francs in fees compared to a traditional bank solution.

With an investment amount of 400,000 francs, your extra earnings in just 5 years will amount to over 22’000 francs. In other words: Over 22,000 francs that go into your account instead of the bank’s pockets.

Calculate your own savings potential with our Fee Savings Calculator.

Mistake 4: Not taking enough time and/or not getting a second opinion

This is a large amount, and it’s definitely worth investing enough time to find the right solution. Start comparing providers early and never just accept the first offer from your bank. At least two different offers should be compared.

Conclusion

Take the time you need and create a financial overview for your retirement – even a few years in advance. Don’t rely on just one offer; compare different options. Pay attention to fees, transparency, simplicity, and clarity.

Incorporate your pension fund money in a structured way into your wealth plan and choose a smart investment solution to implement it. This way, you’ll save thousands of francs in fees and delegate the work. Above all, you’ll secure financial freedom and flexibility in your well-deserved retirement.

This might also interest you

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent