Investing money in Switzerland: Tips for beginners

Here’s how you can invest your money in Switzerland as a beginner

Are you looking for some advice on how to invest your money in Switzerland? Then you’ve come to the right address. We have summarised the most important facts for you on how to invest your money and what you should bear in mind. In order to minimise the risk of investing money, it is important that you invest your money in a diversified way. This means that you invest broadly in different assets instead of putting all your eggs in one basket. Investing money as a beginner and achieving high returns is easier than you think. Our mission at findependent is to make investing in Switzerland easy and understandable, so that even beginners can invest money comfortably.

That’s why we have summarised the most important facts for beginners on how to invest money in Switzerland.

Before you start, we explain the different forms of investment.

Here you can navigate to the following questions:

What types of investments do exists?

Investing in shares

With an investment in shares you invest directly in a company. As a share owner, you hold shares and are thus a co-owner of a company and in return receive a part of the profit in the form of dividends. The profit prospects of shares are promising in the long term, but they are also subject to fluctuations. In order to balance out the fluctuations of the stock market, a diversified investment is important.

Investing in bonds

When you invest money in bonds, you hold shares in large loans to the government or companies. Bonds have a fixed term during which you receive interest. Bonds are often also called loans. Bonds are particularly suitable as a safe investment product, but also have lower profit prospects compared to shares.

Fixed-term deposit investments

A time deposit is a bit of a relic from times gone by. Those were the times when interest rates were high and banks paid considerable rates of interest even for short-term investments. As we all know, those times are long gone. Although there seems to have been a recent shift away from the low interest rate policies of the central banks, this is still not nearly enough for reasonable interest rates on a time deposit in Swiss francs.

Time deposits normally have a maximum term of 12 months. What is particularly striking is the high minimum investment, which varies from bank to bank but is usually around 100,000 Swiss francs.

There are hardly any risks involved in a time deposit. Only if the money has to be available before the end of the agreed term, i.e. prematurely, are there problems. In most cases, substantial “penalty interest” is then charged. If you can wait for the term to expire, you get the total amount including interest back at the end. If, for example, 0.10% interest has been agreed for a term of 6 months, the invested amount including interest will be returned after 6 months. The interest rate is usually defined as the annual interest rate, not broken down to the term. In concrete terms, this means: 0.05% for 6 months.

Fixed-term deposits and fiduciary deposits are also available in foreign currencies. Here it is important to be aware of the foreign currency risk. And the counterparty risk. Often the money in a fiduciary deposit is no longer held by the bank’s Swiss stock company but by a subsidiary, e.g. in the British Virgin Islands or Guernsey.

Objectively speaking, time deposits are not a sensible long-term investment instrument.

Precious metals as an investment

Precious metals are one of the oldest forms of investment. Precious metals refer to gold and silver, for example, and they have a reputation as a safe investment. On the other hand, precious metals do not generate any real returns. The investments have no real added value for the real economy and are also rather questionable from a sustainable point of view, as the mining of precious metals sometimes damages the environment.

Real estate investment

As a real estate owner, you are co-owner of real estate and receive a rent for it. Real estate is also a good way to diversify a portfolio. Large sums of money are usually required to purchase real estate, because the prices of real estate in Switzerland are high.

Investing in ETFs

ETFs (exchange traded funds) are funds traded on the stock exchange and are suitable for investing in an entire stock, bond or real estate market. Investing in ETFs makes it possible to invest broadly with small amounts, because an ETF pools the money of many investors and uses it to buy shares, bonds or real estate. Another advantage is the low fees. Due to the possibility of investing small amounts on a broad basis and at low fees, ETFs are particularly well suited to start investing money.

Depending on the ETF, the income is used differently. A distinction is made between distributing and accumulating ETFs.

What types of investments do exists?

Investing in shares

With an investment in shares you invest directly in a company. As a share owner, you hold shares and are thus a co-owner of a company and in return receive a part of the profit in the form of dividends. The profit prospects of shares are promising in the long term, but they are also subject to fluctuations. In order to balance out the fluctuations of the stock market, a diversified investment is important.

Investing in bonds

When you invest money in bonds, you hold shares in large loans to the government or companies. Bonds have a fixed term during which you receive interest. Bonds are often also called loans. Bonds are particularly suitable as a safe investment product, but also have lower profit prospects compared to shares.

Fixed-term deposit investments

A time deposit is a bit of a relic from times gone by. Those were the times when interest rates were high and banks paid considerable rates of interest even for short-term investments. As we all know, those times are long gone. Although there seems to have been a recent shift away from the low interest rate policies of the central banks, this is still not nearly enough for reasonable interest rates on a time deposit in Swiss francs.

Time deposits normally have a maximum term of 12 months. What is particularly striking is the high minimum investment, which varies from bank to bank but is usually around 100,000 Swiss francs.

There are hardly any risks involved in a time deposit. Only if the money has to be available before the end of the agreed term, i.e. prematurely, are there problems. In most cases, substantial “penalty interest” is then charged. If you can wait for the term to expire, you get the total amount including interest back at the end. If, for example, 0.10% interest has been agreed for a term of 6 months, the invested amount including interest will be returned after 6 months. The interest rate is usually defined as the annual interest rate, not broken down to the term. In concrete terms, this means: 0.05% for 6 months.

Fixed-term deposits and fiduciary deposits are also available in foreign currencies. Here it is important to be aware of the foreign currency risk. And the counterparty risk. Often the money in a fiduciary deposit is no longer held by the bank’s Swiss stock company but by a subsidiary, e.g. in the British Virgin Islands or Guernsey.

Objectively speaking, time deposits are not a sensible long-term investment instrument.

Precious metals as an investment

Precious metals are one of the oldest forms of investment. Precious metals refer to gold and silver, for example, and they have a reputation as a safe investment. On the other hand, precious metals do not generate any real returns. The investments have no real added value for the real economy and are also rather questionable from a sustainable point of view, as the mining of precious metals sometimes damages the environment.

Real estate investment

As a real estate owner, you are co-owner of real estate and receive a rent for it. Real estate is also a good way to diversify a portfolio. Large sums of money are usually required to purchase real estate, because the prices of real estate in Switzerland are high.

Investing in ETFs

ETFs (exchange traded funds) are funds traded on the stock exchange and are suitable for investing in an entire stock, bond or real estate market. Investing in ETFs makes it possible to invest broadly with small amounts, because an ETF pools the money of many investors and uses it to buy shares, bonds or real estate. Another advantage is the low fees. Due to the possibility of investing small amounts on a broad basis and at low fees, ETFs are particularly well suited to start investing money.

Depending on the ETF, the income is used differently. A distinction is made between distributing and accumulating ETFs.

ETFs

- Distributing ETFs pay out the income

- Accumulating ETFs reinvest the income

findependent invests in accumulating ETFs when investing abroad in order to save on exchange rate costs, stock exchange and stamp duties. Fees are charged when income is converted into Swiss francs and exchanged back into the foreign currency when invested.

Investing money in funds

As with an ETF, the money in a fund is invested in a bundle and is therefore suitable for a diversified investment. Unlike ETFs, traditional funds are not traded on the stock exchange, but can be sold or bought once a day at the bank. Most funds pursue an active investment strategy and often have high fees that investors are not always aware of.

Investing money in crypto

Cryptocurrencies are digital currencies such as Bitcoin, Ethereum or Ripple. Cryptocurrencies are currently in vogue, but there are also many critics and the future development is difficult to predict. A crypto investment is therefore associated with high risks.

Foreign currency investments

Investing in foreign currencies is also called foreign exchange trading and takes place in the exchange between different foreign currencies. The investor hopes to buy the foreign currency at a lower price and sell it again at a higher price. Foreign exchange trading is not suitable for private individuals, but it is for companies, depending on the situation.

Conclusion

There are many ways to invest money. It is important that you diversify your portfolio so that your risk of losing money is reduced as much as possible. ETFs are the perfect way to invest your money with low risk and broad diversification. With an ETF, even small amounts can be invested worldwide in shares, bonds or real estate. With findependent you can invest your savings wisely instead of keeping your money in a savings account with low interest rates. From CHF 500, you can invest money easily and without prior knowledge, and the investment strategy tailored to you is also suitable for beginners and makes investing money in Switzerland possible at fair fees. You can also invest the first CHF 2,000 for a lifetime without management and custody fees.

We have 6 tips for investing money in Switzerland.

Scan the QR code and get the findependent investment app on your smartphone!

Get the findependent investment app on your smartphone!

![]()

![]()

What should you look out for when investing?

You have now learned about many different types of investment. The options for investing money are huge and all have their pros and cons, depending on your needs. But before you start investing, there are a few things you should consider and the most common investment mistakes you should avoid. We have therefore summarised 6 tips for investing money in Switzerland:

1. Determine your investment profile

Your investment type depends, among other things, on your risk tolerance. We have put together various investment solutions for you so that you can invest your money in a way that suits your investment type. You can simply fill out a digital questionnaire and you will automatically receive an investment proposal. It is up to you whether you want to accept the proposal or choose a different investment solution. The different investment solutions vary according to the type of investment split between shares, bonds and real estate. Shares have a promising prospect of a high return, but they are also subject to fluctuations and have a higher risk of loss. Since shares are considered rather risky, the share of shares is correspondingly higher for risk-loving than for prudent investors. The higher the proportion of shares, the higher the expected return, but the higher the loss in a crisis.

If your risk tolerance changes due to a change in your life situation, for example due to retirement, you can also change your investment solution at findependent at any time. However, a change of investment strategy should be carefully considered, as this may lead to high transaction costs. A change of investment solution due to short-term fluctuations of individual asset classes is therefore not worthwhile.

Find your personal investment solution at findependent that matches your risk tolerance.

What should you look out for when investing?

You have now learned about many different types of investment. The options for investing money are huge and all have their pros and cons, depending on your needs. But before you start investing, there are a few things you should consider and the most common investment mistakes you should avoid. We have therefore summarised 6 tips for investing money in Switzerland:

1. Determine your investment profile

Your investment type depends, among other things, on your risk tolerance. We have put together various investment solutions for you so that you can invest your money in a way that suits your investment type. You can simply fill out a digital questionnaire and you will automatically receive an investment proposal. It is up to you whether you want to accept the proposal or choose a different investment solution. The different investment solutions vary according to the type of investment split between shares, bonds and real estate. Shares have a promising prospect of a high return, but they are also subject to fluctuations and have a higher risk of loss. Since shares are considered rather risky, the share of shares is correspondingly higher for risk-loving than for prudent investors. The higher the proportion of shares, the higher the expected return, but the higher the loss in a crisis.

If your risk tolerance changes due to a change in your life situation, for example due to retirement, you can also change your investment solution at findependent at any time. However, a change of investment strategy should be carefully considered, as this may lead to high transaction costs. A change of investment solution due to short-term fluctuations of individual asset classes is therefore not worthwhile.

Find your personal investment solution at findependent that matches your risk tolerance.

2. Diversify your investment portfolio

In order to take as little risk as possible when investing, it is important to diversify your portfolio. Diversification means investing in as many different assets as possible and not just in individual companies, sectors or even countries. In this way you avoid becoming reliant on individual investments. With findependent, you can invest in ETFs with a broad base even with small amounts. As you have already learned, with an ETF you invest in an entire stock, bond or real estate market, which reduces your risk.

To ensure that the investments are actually broadly based, there are a few things to bear in mind when selecting ETFs. Although the allocation to Swiss equities is attractive in terms of tax and foreign currency costs, they are also dependent on individual sectors, such as the pharmaceutical industry with companies like Novartis and Roche. In order to achieve geographical and sector diversification, the equity component of the findependent investment solution is invested 40% in Switzerland and 60% abroad. The main objective of the bond asset class is stability. To ensure that the fluctuation in value of the investment solution remains bearable even during a crisis, a bond component is important. findependent invests 80 % in Swiss corporate bonds and 20 % in emerging market bonds in USD. The real estate portion, on the other hand, is invested entirely in Switzerland. Investments are made in both residential and commercial buildings. Here, too, the aim is to bring stability to the portfolio. The strong Swiss real estate market is ideal for this. So our first tip for investing for beginners is: diversify your portfolio!

3. Start early

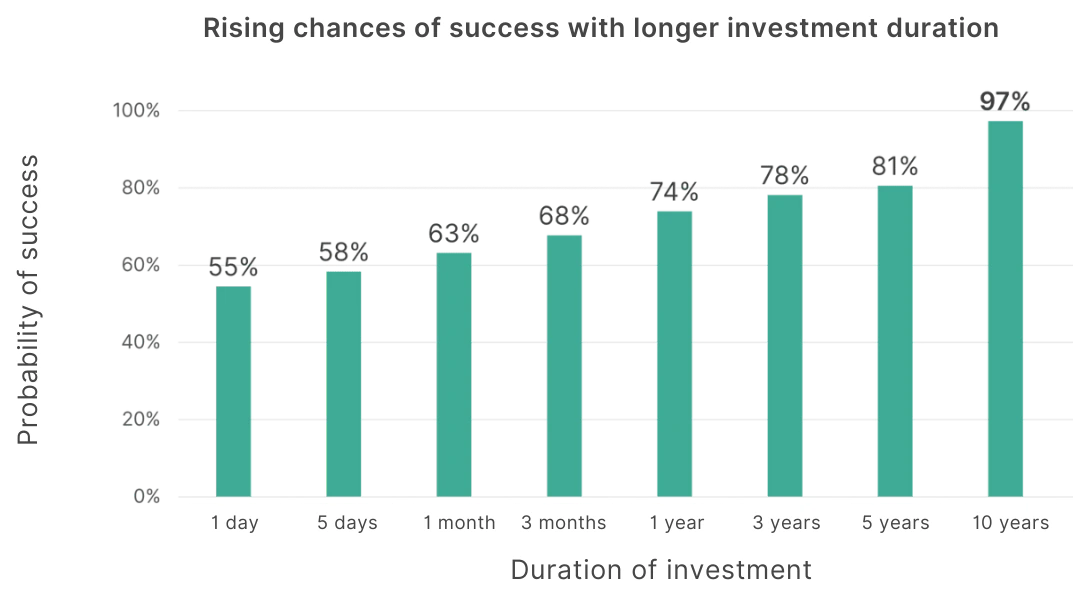

Our second tip is to start investing as early as possible! The earlier you start investing your money, the more likely you are to benefit from a high return in the long term. An important factor for successful returns is the compound interest effect. It contributes to the fact that your assets grow faster and faster with a longer investment period. In addition, the probability of making a loss on an investment decreases over time. This means that the chances of success increase with a long investment period. If you look at the historical performance of the Swiss stock market, you will see that the stock market has increased by a factor of twelve. In between, there have always been phases with losses, such as the Corona crisis in 2020 or the financial crisis in 2008. Financial markets are subject to fluctuations, but they also recover again. Booms and crises are part of this to a certain extent, which is why investment prices often wave upwards over the years. In the long term, there is economic growth and therefore, among other things, share prices rise. You now know that it pays to invest early.

2. Diversify your investment portfolio

In order to take as little risk as possible when investing, it is important to diversify your portfolio. Diversification means investing in as many different assets as possible and not just in individual companies, sectors or even countries. In this way you avoid becoming reliant on individual investments. With findependent, you can invest in ETFs with a broad base even with small amounts. As you have already learned, with an ETF you invest in an entire stock, bond or real estate market, which reduces your risk.

To ensure that the investments are actually broadly based, there are a few things to bear in mind when selecting ETFs. Although the allocation to Swiss equities is attractive in terms of tax and foreign currency costs, they are also dependent on individual sectors, such as the pharmaceutical industry with companies like Novartis and Roche. In order to achieve geographical and sector diversification, the equity component of the findependent investment solution is invested 40% in Switzerland and 60% abroad. The main objective of the bond asset class is stability. To ensure that the fluctuation in value of the investment solution remains bearable even during a crisis, a bond component is important. findependent invests 80 % in Swiss corporate bonds and 20 % in emerging market bonds in USD. The real estate portion, on the other hand, is invested entirely in Switzerland. Investments are made in both residential and commercial buildings. Here, too, the aim is to bring stability to the portfolio. The strong Swiss real estate market is ideal for this. So our first tip for investing for beginners is: diversify your portfolio!

3. Start early

Our second tip is to start investing as early as possible! The earlier you start investing your money, the more likely you are to benefit from a high return in the long term. An important factor for successful returns is the compound interest effect. It contributes to the fact that your assets grow faster and faster with a longer investment period. In addition, the probability of making a loss on an investment decreases over time. This means that the chances of success increase with a long investment period. If you look at the historical performance of the Swiss stock market, you will see that the stock market has increased by a factor of twelve. In between, there have always been phases with losses, such as the Corona crisis in 2020 or the financial crisis in 2008. Financial markets are subject to fluctuations, but they also recover again. Booms and crises are part of this to a certain extent, which is why investment prices often wave upwards over the years. In the long term, there is economic growth and therefore, among other things, share prices rise. You now know that it pays to invest early.

4. Invest money regularly

You probably hear it over and over again: investing money as early and regularly as possible pays off. Therefore, our tip for beginners is to invest money regularly. But how high should the monthly investment amount be? That depends entirely on your personal financial situation. First of all, it is important that you have a spare of 3 to 6 months’ expenses so that you have enough savings for unforeseen events and are liquid. You should also not need your invested money for the next 5 years. This means that you should not invest your money for larger expenses, such as a new car, a longer trip or further education. This way you avoid selling your investments at an unfavourable time.

On the other hand, how much money you can invest each month also depends on the amount you save each month. We also advise you to consider the ratio of your investment assets to the assets in your savings account. This helps you to keep a balance between return and security. To invest money on a monthly basis, you can set up a regular transfer order for automatic investment. This way you won’t be tempted to spend the money and it will be easier for you to save. It’s better to make small staggered contributions and withdraw money in equal steps.

5. Compare the fees

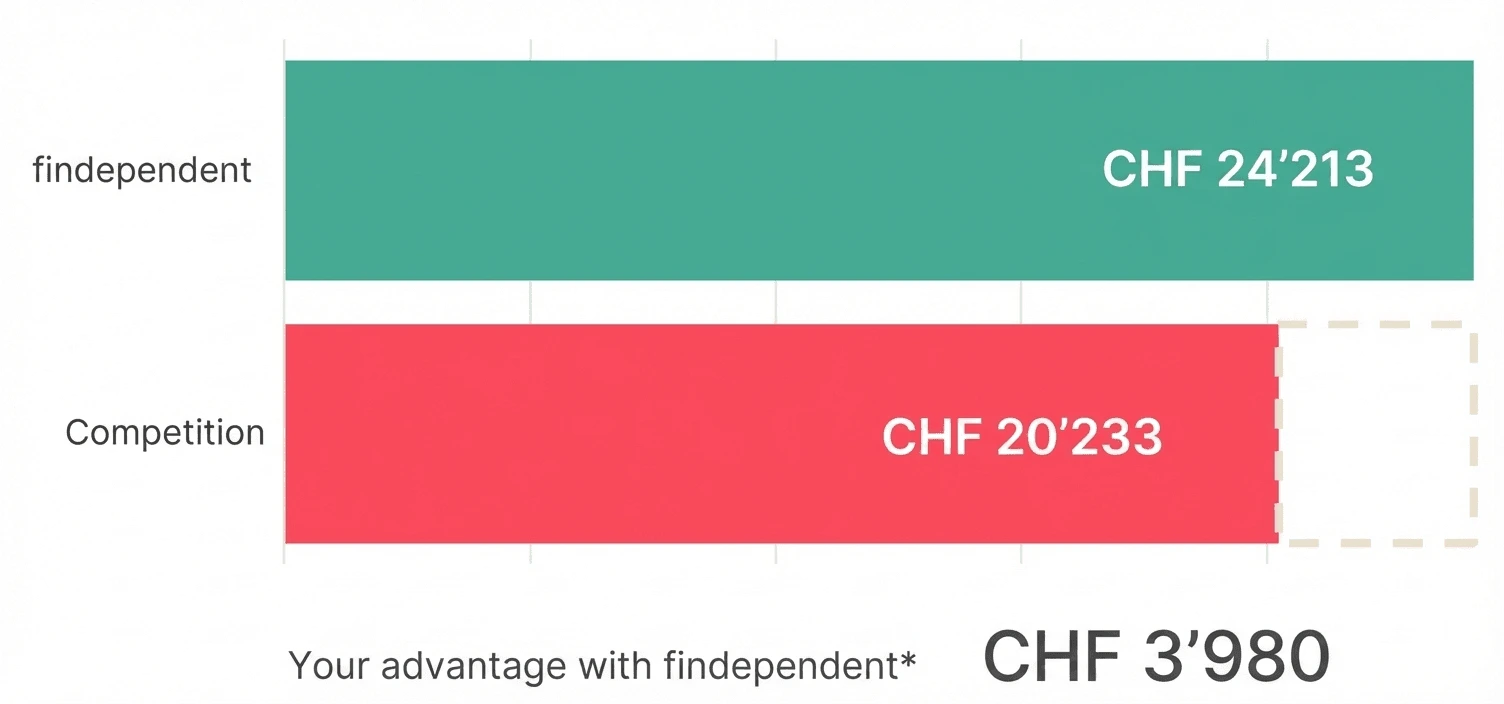

Despite the current low interest rates, you can invest your money wisely. Thanks to lower fees, a higher return remains for you, because high fees reduce your return. A study conducted by the comparison portal moneyland.ch found that asset management mandates are too expensive at many banks and that there is considerable savings potential for clients. “Extrapolated to all Swiss clients, this results in a savings potential of 2.026 billion Swiss francs.” That’s why it’s even more important to compare fees. When you compare investment offers, you will see different custody and management fees on the assets under management of the investment. Even if one per cent doesn’t look like much at first glance, in the long run they cut into your returns. The fees for your investment become more and more noticeable over time. As a comparison, let’s take the average costs of 1.4 % for the investment of 10,000 Swiss francs in Switzerland (study by moneyland.ch) and the expected assets in 20 years. As you can see, with findependent’s investment solution you can clearly profit more from your investment compared to the competition and therefore our tip for investing is: compare the fees, e.g. here.

With an investment at findependent you save around 70 % compared to similar offers. For an investment amount of CHF 10,000, the investment costs less than CHF 80, plus about CHF 30 in product costs. The fee comparison is worthwhile. In addition, with findependent you can invest the first CHF 2,000 without management and custody fees and start with a minimum investment of just CHF 500.

Fees and minimum investment, by the way, are two key figures that are well suited to make the attractiveness of digital asset managers transparent.

4. Invest money regularly

You probably hear it over and over again: investing money as early and regularly as possible pays off. Therefore, our tip for beginners is to invest money regularly. But how high should the monthly investment amount be? That depends entirely on your personal financial situation. First of all, it is important that you have a spare of 3 to 6 months’ expenses so that you have enough savings for unforeseen events and are liquid. You should also not need your invested money for the next 5 years. This means that you should not invest your money for larger expenses, such as a new car, a longer trip or further education. This way you avoid selling your investments at an unfavourable time.

On the other hand, how much money you can invest each month also depends on the amount you save each month. We also advise you to consider the ratio of your investment assets to the assets in your savings account. This helps you to keep a balance between return and security. To invest money on a monthly basis, you can set up a regular transfer order for automatic investment. This way you won’t be tempted to spend the money and it will be easier for you to save. It’s better to make small staggered contributions and withdraw money in equal steps.

5. Compare the fees

Despite the current low interest rates, you can invest your money wisely. Thanks to lower fees, a higher return remains for you, because high fees reduce your return. A study conducted by the comparison portal moneyland.ch found that asset management mandates are too expensive at many banks and that there is considerable savings potential for clients. “Extrapolated to all Swiss clients, this results in a savings potential of 2.026 billion Swiss francs.” That’s why it’s even more important to compare fees. When you compare investment offers, you will see different custody and management fees on the assets under management of the investment. Even if one per cent doesn’t look like much at first glance, in the long run they cut into your returns. The fees for your investment become more and more noticeable over time. As a comparison, let’s take the average costs of 1.4 % for the investment of 10,000 Swiss francs in Switzerland (study by moneyland.ch) and the expected assets in 20 years. As you can see, with findependent’s investment solution you can clearly profit more from your investment compared to the competition and therefore our tip for investing is: compare the fees, e.g. here.

Expected savings in 20 years with an investment of CHF 10,000

With an investment at findependent you save around 70 % compared to similar offers. For an investment amount of CHF 10,000, the investment costs less than CHF 80, plus about CHF 30 in product costs. The fee comparison is worthwhile. In addition, with findependent you can invest the first CHF 2,000 without management and custody fees and start with a minimum investment of just CHF 500.

Fees and minimum investment, by the way, are two key figures that are well suited to make the attractiveness of digital asset managers transparent. We have visualised this for you in the chart below:

6. Be patient

Although a few people have become millionaires overnight by investing money, the prospect of getting rich quickly is rather slim. Therefore, our last tip for investing money requires patience. Scientific studies even prove that speculators tend to lose money on the stock market. With long-term investments, you buy broadly based investments and hold them in all market situations. Incidentally, this is also called passive investment. In contrast, speculators invest for the short term and bet on individual stocks, hoping to make quick profits by buying and selling. However, this is very time-consuming and risky.

With a large portion of patience, you will be rewarded with high probability of returns in the long run. With a longer investment period, the risk is reduced, which is why we recommend that you pursue a buy-and-hold strategy. Passive behaviour leads to success in the long term. It’s best not to look at your investment solution too often, but to sit back and let your money work for you. Trust the process!

Patience is the supreme virtue of the investor. – Benjamin Graham

6. Be patient

Although a few people have become millionaires overnight by investing money, the prospect of getting rich quickly is rather slim. Therefore, our last tip for investing money requires patience. Scientific studies even prove that speculators tend to lose money on the stock market. With long-term investments, you buy broadly based investments and hold them in all market situations. Incidentally, this is also called passive investment. In contrast, speculators invest for the short term and bet on individual stocks, hoping to make quick profits by buying and selling. However, this is very time-consuming and risky.

With a large portion of patience, you will be rewarded with high probability of returns in the long run. With a longer investment period, the risk is reduced, which is why we recommend that you pursue a buy-and-hold strategy. Passive behaviour leads to success in the long term. It’s best not to look at your investment solution too often, but to sit back and let your money work for you. Trust the process!

Patience is the supreme virtue of the investor. – Benjamin Graham

Common questions about investing money

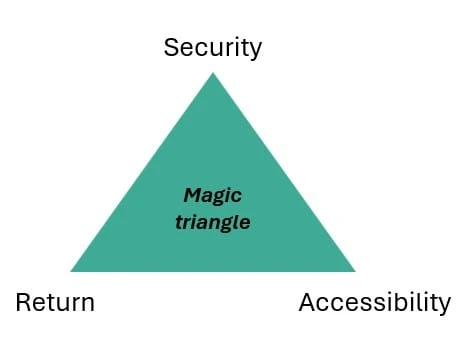

With our 6 most important tips for investing money in Switzerland for beginners, you are now perfectly prepared for the start. We have answered the most important questions for you. First, however, we’ll briefly tell you about the magic triangle: security, accessibility and return. The three goals are in conflict with each other. For example, if you have a high need for security, the return will be correspondingly lower. We explain how the three factors influence your goals and how you can achieve the right combination for you.

Investing money: Risk (security)

Safety refers to how you can preserve your wealth. With a diversified portfolio, you can increase your security by investing your money in a broadly diversified way. It is also important to spread your investments geographically. To determine your personal risk tolerance, you can consider how much temporary loss you can withstand. There are five different risk expectations for the investment solutions at findependent, depending on your risk profile. The lower the equity component of the investment solution, the lower the loss in value in a crisis. However, the expected long-term return is also rather low. With the “risky” investment solution, you would have lost up to 41.7% during the 2008 financial crisis, with the “cautious” investment solution up to 19.4%.

Cautious | Risky |

40% Equity share | 99% Equity share |

-19.4% Biggest annual loss (2008) | -41.7% Biggest annual lost (2008) |

Ø 4.1% Net return per year (2005-2025) | Ø 6.4% Net return per year (2005-2025) |

Investing money: Disposability

Disposability is also called liquidity and becomes important if you need your invested money in a short period of time. For example, investments in non-listed companies such as private equity or start-up (venture capital) usually achieve higher returns than investments in companies traded on the stock exchange. However, the investments cannot be sold for several years and are therefore not readily available. Availability is therefore in conflict with returns.

With findependent you can withdraw your invested money at any time. Nevertheless, we advise you to have a reserve for unforeseen events. The financial buffer helps you to bridge a job change, pay high medical bills or replace a broken device.

Investing money: Interest and return

The return is the profit achieved on your investment solution through the increase in value and the income received (e.g. dividends and interest). Shares, for example, have higher yields, but a correspondingly higher loss in value during a crisis. As already mentioned in connection with the security factor, returns in particular are in conflict with security. With the Risky investment solution, the net return from 2005 to 2021 averaged 6.9% per year, and during the financial crisis of 2008 you would have lost a maximum of -41.7% of your investment sum. If you want to achieve the highest possible return, you must also be able to withstand a high loss in value during a crisis.

Whether you prefer to invest money in Switzerland in a careful, cautious, balanced, brave or even risky manner, you will find an investment solution that suits your personal risk preference at findependent.

Common questions about investing money

With our 6 most important tips for investing money in Switzerland for beginners, you are now perfectly prepared for the start. We have answered the most important questions for you. First, however, we’ll briefly tell you about the magic triangle: security, accessibility and return. The three goals are in conflict with each other. For example, if you have a high need for security, the return will be correspondingly lower. We explain how the three factors influence your goals and how you can achieve the right combination for you.

Investing money: Risk (security)

Safety refers to how you can preserve your wealth. With a diversified portfolio, you can increase your security by investing your money in a broadly diversified way. It is also important to spread your investments geographically. To determine your personal risk tolerance, you can consider how much temporary loss you can withstand. There are four different risk expectations for the investment solutions at findependent, depending on your risk profile. The lower the equity component of the investment solution, the lower the loss in value in a crisis. However, the expected long-term return is also rather low. With the risk-averse investment solution, you would have lost up to 41.7% during the 2008 financial crisis, with the cautious investment solution up to 19.4%.

Cautious | Risky |

40% Equity share | 99% Equity share |

-19.4% Biggest annual loss (2008) | -41.7% Biggest annual lost (2008) |

Ø 4.1% Net return per year (2005-2025) | Ø 6.4% Net return per year (2005-2025) |

Investing money: Disposability

Disposability is also called liquidity and becomes important if you need your invested money in a short period of time. For example, investments in non-listed companies such as private equity or start-up (venture capital) usually achieve higher returns than investments in companies traded on the stock exchange. However, the investments cannot be sold for several years and are therefore not readily available. Availability is therefore in conflict with returns.

With findependent you can withdraw your invested money at any time. Nevertheless, we advise you to have a reserve for unforeseen events. The financial buffer helps you to bridge a job change, pay high medical bills or replace a broken device.

Investing money: Interest and return

The return is the profit achieved on your investment solution through the increase in value and the income received (e.g. dividends and interest). Shares, for example, have higher yields, but a correspondingly higher loss in value during a crisis. As already mentioned in connection with the security factor, returns in particular are in conflict with security. With the Risky investment solution, the net return from 2005 to 2021 averaged 6.9% per year, and during the financial crisis of 2008 you would have lost a maximum of -41.7% of your investment sum. If you want to achieve the highest possible return, you must also be able to withstand a high loss in value during a crisis.

Magic Triangle

Whether you prefer to invest money in Switzerland in a careful, balanced, courageous or even risk-averse manner, you will find an investment solution that suits your personal risk preference atependent.

FAQs – most frequently asked questions about investing money in Switzerland

Now that you know the magic triangle and how the three factors influence your investment, we answer the most important questions for beginners about investing money in Switzerland.

Why should I start investing?

You don’t have to be a professional or rich to invest money wisely. You can start with just a little money and achieve high returns. However, the offers on the internet about investments are huge and it is easy to lose the overview. There are numerous ways to invest money. You are probably wondering how much money you can start with and in which investment forms you can invest. At findependent you can start with as little as CHF 500 and easily invest in ETFs. The advantage of ETFs is that you can invest broadly and therefore diversified. With a long-term investment horizon of at least 10 years, you would have made a profit of 97% on the Swiss stock market, and CHF 1,000 would have turned into CHF 2,310 on average. As you can see, it already pays to invest a little money. If you save an additional amount every month, you can invest the money every month instead of leaving it in a savings account. Investing money early pays off because your invested money keeps growing and benefits from compound interest. Compound interest is interest paid on interest income. Over a longer period of time, the interest-bearing capital increases exponentially (i.e. at an ever steeper rate). The interest is therefore reinvested, or rather retained. The compound interest effect happens faster and faster over time and therefore the invested capital increases enormously.

How and where is it best to invest money?

It is best to invest your money in a wide range of companies and real estate worldwide. Investments in shares, bonds and real estate are suitable for this purpose in order to benefit from regular returns.

So that you don’t have to deal with the financial markets all the time, we have created 4 ready-made investment solutions at findependent. All investment solutions are diversified and sustainable, so that you can invest your money with the highest possible return. With findependent you can invest your money in Switzerland with as little as CHF 500.

What is the best way to invest 10,000 Swiss francs?

We recommend that you start investing as early as possible with small amounts on an ongoing basis. It is therefore best to invest CHF 10,000 in stages, regardless of the current market situation. Scientific studies have shown that it is almost impossible to catch the perfect moment. We do not recommend leaving your money in a savings account at the moment because of the low interest rates.

Where can I get the highest return for my investment?

The higher the proportion of shares, the higher the expected return. On the other hand, a possible loss in a crisis is correspondingly higher than with a low share of equities. A high return is therefore associated with high risk and low security. The average return per investment profile varies depending on the investment solution. In the case of findependent’s Risky investment solution, you hold an equity component of 99% and thus also the highest return to be expected in the long term.

How should I divide my assets?

The distribution depends on various factors. On the one hand you should have a reserve for 3 to 6 monthly expenses and on the other hand you should not invest money for planned expenses. Then the allocation depends on your risk profile. The higher your risk tolerance, the more money you can invest. For example, you can invest CHF 30,000 of your assets and leave CHF 20,000 in your savings account. That way you have invested your assets 3:2. With our practical guide, you can find out how to divide your assets.

How can I earn money quickly?

Admittedly, you are probably not alone in wanting to get rich overnight. Unfortunately, the probability of becoming rich overnight is very small. Therefore, you need to be patient in order to build up your wealth. Wealth accumulation takes time and is more like a marathon than a sprint. This is because your investments grow, among other things, due to increasing economic growth. A long investment period is crucial for investment success. This is because the probability of achieving a higher profit and preferably no loss increases with the investment horizon.

How do I invest my money sustainable?

Sustainable investment is an important topic and also a major concern for us. However, everyone understands sustainability differently. You start to deal with the question, what is sustainable investing anyway and how is it measured? Investing money with findependent is not only worthwhile financially, but you can also stand behind your investments. We use so-called ESG Screened ETFs for foreign equity investments. ESG stands for (Environmental Social Governance) and means environment, society and corporate governance. The ETFs only invest in companies that adhere to the UN Global Compact and exclude companies from the nuclear power, coal power, coal mining, oil sand mining, tobacco industry, nuclear, controversial (e.g. cluster munitions) and civilian weapons sectors. The UN Global Compact was adopted to make globalisation social and ecological. If you want to know more about the exact criteria for an ESG Screened ETF, you can find detailed information here.

Now you know not only how to invest smartly, but also how to invest sustainably and achieve a high return.

How much does it cost to invest money?

Traditional asset management is rather expensive and only possible with large amounts. Fortunately, there are now robo-advisors that make investing possible for everyone! A robo-advisor makes it possible to manage your investments at low cost and with a low starting amount. But robo-advisors also cost different amounts. It’s best to compare the different offers so that you can find the right one for you. Basically, there are management and custody fees. In addition, however, there are product costs, the so-called TER. You are probably wondering what TER means. TER is the abbreviation for Total Expense Ratio and is the total expense ratio of your ETF. If you invest in an ETF in a foreign currency, there are exchange rate surcharges. Stamp duties for the tax authorities and stock exchange duties for the Swiss stock exchange also apply. Based on your investment amount, you will be charged quarterly 0.10% management and custody fees (0.40% p.a. or less). In addition, findependent tries to keep costs low with as few transactions as possible. Perhaps you have heard of the stock market saying, “Back and forth makes pockets empty”. The stock market expert André Kostolany meant by this that the transaction costs add up with many purchases and sales. Everything clear so far?

It is important that you take a close look at the fees and compare them, because the lower the fees, the more is left for you and your goals.

Transparency in fees is very important to us. With findependent you can also start with up to CHF 2,000 without management and custody fees.

With our fee calculator you can calculate the costs for your personal situation. Transparent and simple.

When is the best time to invest money?

You’ve probably heard someone tell you that now is the perfect time to invest and wondered if you’re missing the right moment? We can reassure you – there is no such thing as the perfect time – this is proven by several studies. Depending on future forecasts, supply and demand on the financial markets change. This means that you have to remain calm and relaxed in stormy times and that you should invest continuously and not all at once. This way you can also benefit from a long-term increase in value. If you want to invest CHF 20,000, for example, we recommend that you invest the money in stages over 1-2 years.

If you regularly read the news about what is happening on the financial markets, you will quickly find yourself speculating and falling into a psychological trap. Don’t go crazy – doing nothing is almost always the best reaction, because the buy and hold strategy is more promising in the long run. As mentioned earlier, frequent buying and selling costs money.

Time in the market beats timing the market!

What are the best ETFs for beginners?

The more broadly based the ETF invests, the better. In this respect, the Vanguard FTSE All World would be a good option. However, this ETF invests over 60% in the USA and only 2% in Switzerland. The ETF is managed in USD, so you are subject to exchange rate fluctuations between the US dollar and the Swiss franc.

A broad-based ETF portfolio, such as the findependent investment solutions, is therefore more suitable for beginners.

Which shares to buy for beginners?

As a beginner, you should not just buy individual shares, but rather invest in a broad-based equity ETF.

How do you get rich?

You won’t get rich overnight with a broad-based investment, but you will build up a fortune over time. Start with 10,000 francs, deposit 800 francs every month and after 15 years you will have a quarter of a million francs (250,000).

Which investment is worthwhile?

Any investment in a broad-based investment solution is worthwhile in the long term. Pay attention to low and transparent costs, simple handling and a balanced asset allocation.

How long will CHF 500,000 last after retirement?

It depends on how high the cost of living is and whether the CHF 500,000 is at least partially invested in an investment solution instead of sitting in a savings account.

Scan the QR code and get the findependent investment app on your smartphone!

Start now and get the findependent investment app on your smartphone!

![]()

![]()

These are the alternatives to investing

In addition to investing money using the inexpensive and simple investment app from findependent, there are various alternatives. We explain their advantages and disadvantages.

Investing or spending money

Spending money and thus keeping the economy going is certainly not completely wrong. Besides, you have to spend money anyway to finance your life. It is important that you not only think in the present, but also plan for the future. You always think about major purchases (house, travel, education, time off, part-time work, retirement, etc.) some time in advance. This is the time when you should start putting money aside for these purchases at the very latest. Putting money aside means, since the savings account does not yield any interest, investing money in a smart, cheap and simple investment solution.

Investing money or buying real estate

Buying a property can also be a form of investment. But often you then tie up most or even all of your savings in this one form. And putting all your eggs in the same basket is not a good idea. Once you have bought the property and are using it yourself, you have additional security, because no landlord can give you notice. And a home of your own is ultimately also a piece of freedom. In addition to your own savings, a property is financed with a bank loan called a mortgage. This mortgage costs mortgage interest. In addition, there are ancillary costs, maintenance work and provisions for renovations. And finally, the value of the property also varies. Of course, the owner is hardly concerned about this as long as he or she does not want to sell the property and does not receive an additional payment from the bank on top of the mortgage.

Investing money or paying off the mortgage

Have you taken out a fixed-rate mortgage and now you want to repay it at an earlier date? Your bank is seldom happy about this and will punish you with a penalty in the form of an early repayment fee. It is therefore better to make repayments at the end of the term of a fixed-rate mortgage or money market mortgage. But even then, you should think carefully about whether you can achieve more return than the mortgage interest to be paid with a long-term investment strategy. You should also include tax considerations in the calculation.

Investing or saving money

Investing money is the new saving. Because savings accounts pay little or no interest and inflation is now everywhere. You should therefore invest money that you won’t need for several years or that you have earmarked in a smart investment solution. Interest rates on savings accounts are zero or just above zero. The savings account has definitely had its day. Money you don’t need in the long term should be invested. In this way, you also protect it from the gradual devaluation caused by inflation.

Invest money or buy gold

Gold is considered a safe haven, but that is probably more myth than reality. The fluctuations in value are considerable. Between 2018 and 2020, the price rose from just under USD 1,200 to around USD 2,000, only to return to around USD 1,700 in mid-2022. Gold can make sense as a discreet addition or play money. It should not be a central component of your portfolio.

Investing money or paying off debts

If you have money available and are thinking about investing it, but at the same time you have debts elsewhere, it is probably best to pay off the debt first. By the way, this does not apply to the mortgage mentioned above; here the situation is somewhat more complex. Debts in the form of loans between friends, acquaintances or specialised companies often carry interest rates that are much higher than the expected return on investment. If this is not the case, or if you have an interest-free loan, you can invest your money safely. Just keep in mind that when investing, it is important to stick to your investment horizon in order to achieve the expected long-term return and not to have to sell at the worst possible moment. The lender must therefore be able to assure you that he/she will not call in the debt at an inopportune moment.

Investing money or paying back the loan

A traditional consumer loan usually comes with an expensive interest rate and may have a fixed term. Therefore, first check whether you can make repayments at all outside the scheduled repayment instalments and terms. If this is not the case, you can invest your money, but as always, you should make sure that you have a sufficiently long investment horizon for investing in the financial markets. If you want to repay the consumer loan in 2 years, at the end of its term, you should better leave the money in the savings account. As soon as the investment horizon is several years, five years is a good indication, you can invest your money in a cheap and simple investment solution.

Let’s Get to Know Each Other

If you prefer a more personal touch, you can book a free 30-minute consultation with us. It’s the perfect opportunity to ask any burning questions you have about investing or how findependent works.

Key takeaways on investing money in Switzerland

You have now learned the most important things about investing money and the possibilities in Switzerland. Here we summarise the most important key takeaways so that you can start investing money safely even as a beginner.

- Determine your investment type

- Diversify your portfolio

- Start early

- Invest for the long-term

- Invest money regularly

- There is no perfect time

- Even small amounts pay off

- Costs reduce the return

- Compare fees

- Be patient

We at findependent support you and make investing money in Switzerland possible, even for beginners.

Scan the QR code and get the findependent investment app on your smartphone!

Get the findependent investment app on your smartphone!

![]()

![]()

You might also be interested in

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://stage.findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed?

https://stage.findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed? https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal

https://stage.findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works

https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This

https://stage.findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors

https://stage.findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland

https://stage.findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple!

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple! https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap