How much should I invest?

A practical guide on how to determine your appropriate investment amount

Are you wondering how much money you should invest in your situation? Unfortunately, the answer is not that simple. It depends not only on your current circumstances and financial situation. Your willingness to take risks also plays a role.

Between security and return

On the one hand, when investing for the long term, it is important to invest only the money that you do not want to spend in the next few years. This is so that you don’t suddenly have to sell your investments at a loss at an inopportune time because you no longer have enough liquidity.

On the other hand, the higher return on investment and, above all, the compound interest effect are arguments in favour of investing as much money as possible. Especially with a long investment period, the amount you choose to invest can make a big difference.

For most people, it is important to find the right balance between security and return. Using an example, we will show you how to proceed step by step to determine the optimal amount for you.

Guide based on a simplified example

1. Determine expenses and liquidity

First of all, you need to know how much your regular expenses are and where they go. You should certainly not invest this money.

And because not everything in life always goes according to plan, it makes sense to have a reserve for the unpredictable. This could be repairing the dishwasher, paying off a high medical bill or buying a new mobile phone. As a rule of thumb, a reserve of liquid assets of 3 to 6 months’ wages is recommended. If you have no income for a while, e.g. if you change your job and become unemployed, you could bridge this gap.

To this reserve in the savings account, you should also add larger future expenses that have already been determined, such as a planned car purchase, a longer trip or further education. Basically, we recommend the following: Do not invest the money for the definitely planned expenses of the next 3-5 years. This way you can significantly reduce the risk of making a loss with your investments.

But what do you do with future plans and expenses that are not yet completely clear? Here it is advisable to consider how high the probability is that you will spend larger amounts of money. If a goal such as buying a house is still in the distant future, it makes more sense to invest the savings for this purpose. If, on the other hand, you might have to buy a new car soon, you should have at least part of it in your savings account.

Nora has CHF 50,000 in savings and an income of CHF 6,000 per month. She now wants to invest money for her future.

Nora calculates that her monthly expenses amount to about CHF 5,000. This means that she can currently save an average of CHF 1,000 per month.

She knows that she would like to spend a total of about CHF 5,000 of her savings on new furniture in the near future. However, because this wish can easily be paid for with about three months’ wages, Nora does not build up a reserve for it. If she were to become unexpectedly unemployed, she could well do without the new furniture for the time being.

Besides, buying a house is a dream of hers that she wants to save for. Thinking about it, Nora quickly realises that she will probably not be able to fulfil this dream for at least 7 years. This means that buying a house today has no influence on her investment amount.

For Nora, the rule of thumb of liquidity means that she should have CHF 18,000-36,000 as a reserve in her savings account and so she comes to the conclusion that she could theoretically invest CHF 14,000-32,000 of her assets (the CHF 50,000) at present.

2. Compare returns

Now you already know in which spectrum your suitable investment amount is and next you want to find out where exactly. In this consideration, the opposites of “security” and “return” mentioned at the beginning of the article are opposed to each other.

The example gives you a feeling for how high the differences in return can be due to the compound interest effect.

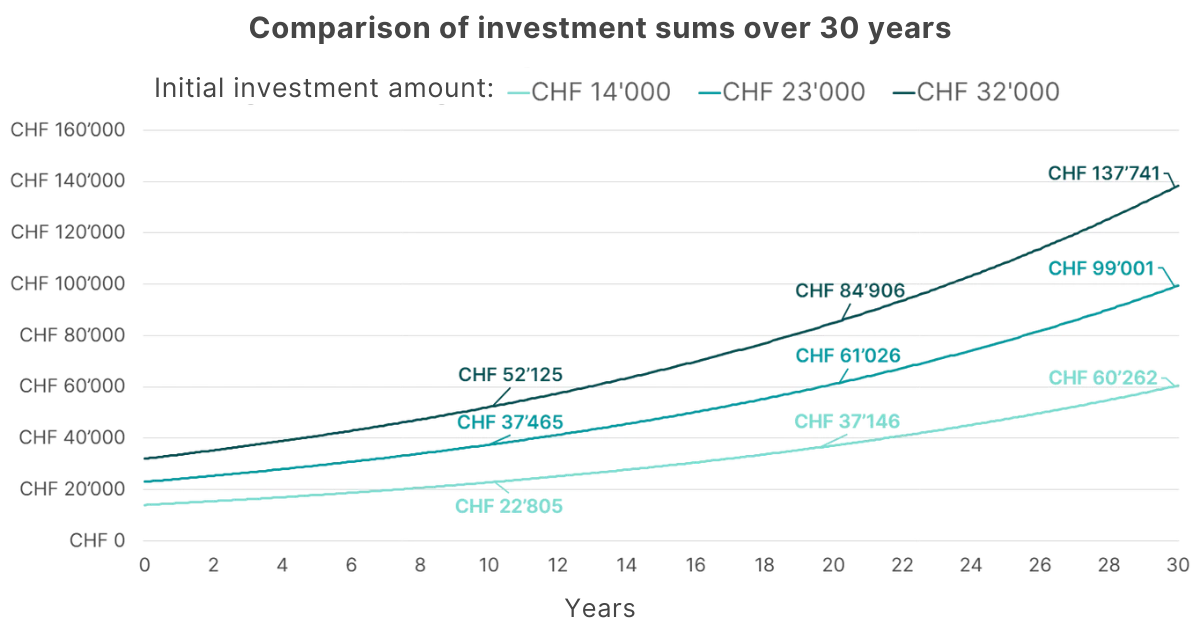

In Nora’s case, the differences between investing CHF 14,000 or CHF 32,000 or, for example, the amount exactly in the middle, look as follows over time:

Comparison of returns over 30 years with different investment amounts at the beginning with an annual return of 5%. (This return corresponds to the approximate historical performance of the findependent investment solution Balanced between 2005 and 2021. However, this is no guarantee for future market developments).

–

Because Nora tends to be a risk adventurer and therefore gives more weight to returns than to security, she opts for a solution more at the upper end of her spectrum: she considers an investment amount of CHF 30,000 to be suitable for her.

Calculate your personal compound interest effect with our compound interest calculator.

3. Assess risk tolerance

As a next step, it is important that you try a little thought experiment. The idea is to find out how high temporary losses you can personally withstand when investing. After all, the value of your investment solution will fluctuate over the years – to varying degrees depending on the proportion of shares in the investment solution – and temporary losses of 30% or even 50% are quite possible in extreme situations. Under no circumstances do you want to sell your investments at rock-bottom prices in times of crisis because you can no longer bear the loss.

So Nora imagines if she could handle it if at one point her investments were only worth around CHF 15,000 instead of CHF 30,000. Could she watch the value fall day by day? Would she still be able to sleep peacefully? Would she hold on to the investments?

For Nora it is now clear: a temporary loss of up to CHF 15,000 is bearable for her. So she decides to invest CHF 30,000 of her CHF 50,000 savings and to keep CHF 20,000 in her savings account as a hedge. Nora’s ratio of investment assets to assets in the savings account is therefore 3:2.

4. Determine the use of additional income

You have already decided how much of your assets you want to invest. Do you still have some of your salary left at the end of each month and can therefore save more on an ongoing basis? Then the next question is how much of your income you would like to invest in addition.

This is again a question of risk tolerance and the balance between return and security. On the one hand, it is most profitable if you stay with the calculated reserve in the savings account and invest everything you have left at the end of the month. On the other hand, this also means that your invested assets – especially in relation to your non-invested assets – will increase considerably over time and you will have to ask yourself how much temporary loss you can mentally cope with. It is important to think a little more long-term and also take into account changes that could play a role in the future.

As a reminder, Nora has decided to keep about 2/5 (CHF 20,000) of her total CHF 50,000 in savings in the savings account and to invest about 3/5 (CHF 30,000). In addition, Nora can save an extra CHF 1,000 each month with her current salary.

So she is now faced with the decision of what to do with this CHF 1,000. Let’s take the following three possible scenarios:

- Scenario 1: She keeps the CHF 30,000 in the investment solution and leaves the entire CHF 1,000 in the savings account.

- Scenario 2: She takes the ratio of investment solution to savings account (3:2) as a guide and invests the same ratio every month, i.e. an additional CHF 600 (3/5 of the CHF 1,000).

- Scenario 3: She keeps the calculated reserve of CHF 20,000 in her savings account and invests the entire additional CHF 1,000 each month.

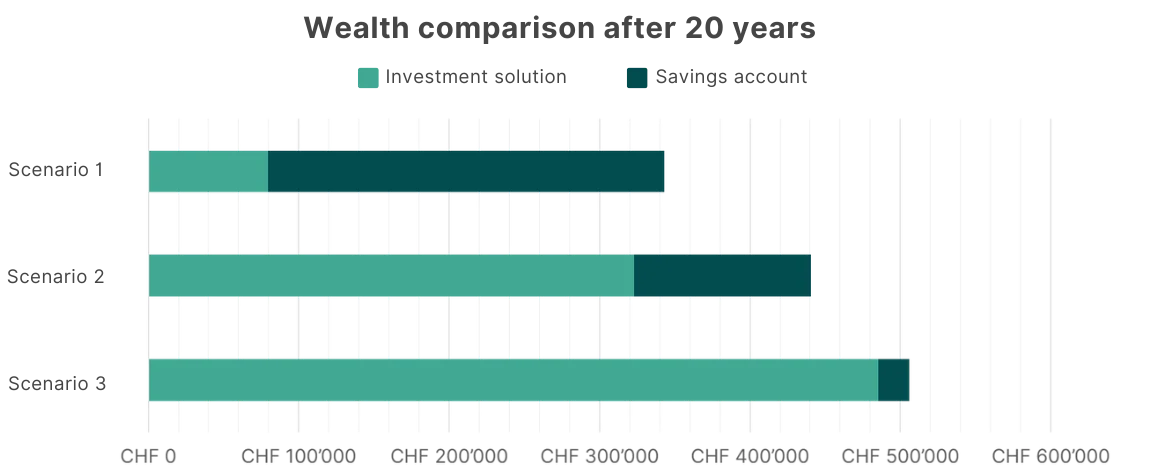

By 20 years from now, the picture would be as follows:

Asset comparison after 20 years with different deposit scenarios at an annual return of 5% for the investment solution and an annual interest rate of 0.12% for the savings account.

–

In the graph, the difference in returns (especially with this long investment period) becomes obvious once again. Thus, Nora could build up about one and a half times as much wealth within 20 years with scenario 3 as with scenario 1.

However, just as much attention should be paid to the security aspect, which is shown by the ratio of investment solution to savings account:

In scenarios 2 and 3, the liquidity portion (savings account) becomes proportionally smaller and smaller over time, while the investment assets and thus also possible temporary losses of the investments become larger and larger. In scenario 3, this is extreme – in the end, around 96% of the total assets are invested there.

Scenario 1 is the safest. The invested assets increase to around CHF 80,000, but the money accumulates mainly in the savings account, which means that after 20 years around 77% of the assets are there.

Nora does not want to accumulate much wealth in her savings account, so scenario 1 is out of the question for her. Scenario 3 is also clearly out of the question for Nora due to the high level of uncertainty. She is just about comfortable with scenario 2, partly because she knows that she will withdraw part of her assets from the investment solution again in around 7-12 years for the desired house purchase. After that, the ratio will shift again. So Nora decides on scenario 2 and with it a rather high amount of CHF 600, which she would like to invest additionally every month.

It is best to pay in and out in stages

Those who react to market developments when investing always lag behind. Trying to hit the “right” times is therefore usually counterproductive – even if many intuitively have the feeling that this is exactly what you need to do to be more successful.

- It’s best to invest your money in staggered amounts – no matter what the market situation looks like at the moment.

- The most convenient way to do this is with a standing order. This way you won’t be tempted to speculate on the “perfect” time and you’ll outsmart yourself, so to speak.

- Finally, withdraw money again in equal steps.

- Good to know: with findependent you have no additional costs for deposits and withdrawals.

Conclusion

The example shown is of course relatively simplified and Nora’s story is not complete in that sense, because life brings many changes.

You, too, should always look at your financial situation and re-evaluate it, especially if there are major changes in your income, your regular expenses, your future goals or your need for security.

If you know yourself and your situation well and feel comfortable investing, then nothing can stand in the way of your personal investment success!

Note: At the moment, neither all pages nor the complete onboarding are available in English. However, we are working intensively to change this. Thank you for your understanding.

You might also be interested in

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent