Inflation in Switzerland

What you can do now to protect your savings

If you’re wondering how best to protect your savings from inflation, you’re not alone. Inflation has been back for some time and is making many everyday goods more expensive. In the meantime (April 2022), inflation in Switzerland was at its highest level for almost 15 years. As at summer 2025, inflation in Switzerland was 0.2% compared to the previous year, with a slight upward trend for the coming years. The purchasing power of your savings is constantly decreasing.

In this blog post, we address the following aspects:

Inflation and salaries in Switzerland

According to the Federal Statistical Office, inflation in 2025, as measured by the national consumer price index, increased by 0.2% compared to the previous year.

Inflation has since fallen back somewhat from the highs of 2022 (+2.5%). In its monetary policy assessment of June 2025, the Swiss National Bank (SNB) wrote: ” Uncertainty regarding the scenario for the global economy remains high.” At the same time, the SNB is raising its warning finger and forecasting higher inflation for the coming years (0.2% for 2025, 0.5% for 2026 and 0.7% for 2027).

However, wages have hardly seen any upward thrust in recent years. Although wages will rise slightly in 2025, there will be hardly any real wage increase left after deducting inflation. Many households continue to feel a loss of purchasing power – particularly due to rising health insurance premiums and the cost of living.

Inflation in Switzerland is therefore gradually devaluing your hard-earned and saved money in private and savings accounts. As a result, you can buy far fewer products/goods with the same amount of Swiss francs than you could a year ago. Inflation increases, your purchasing power decreases.

Deposits in accounts are a losing proposition

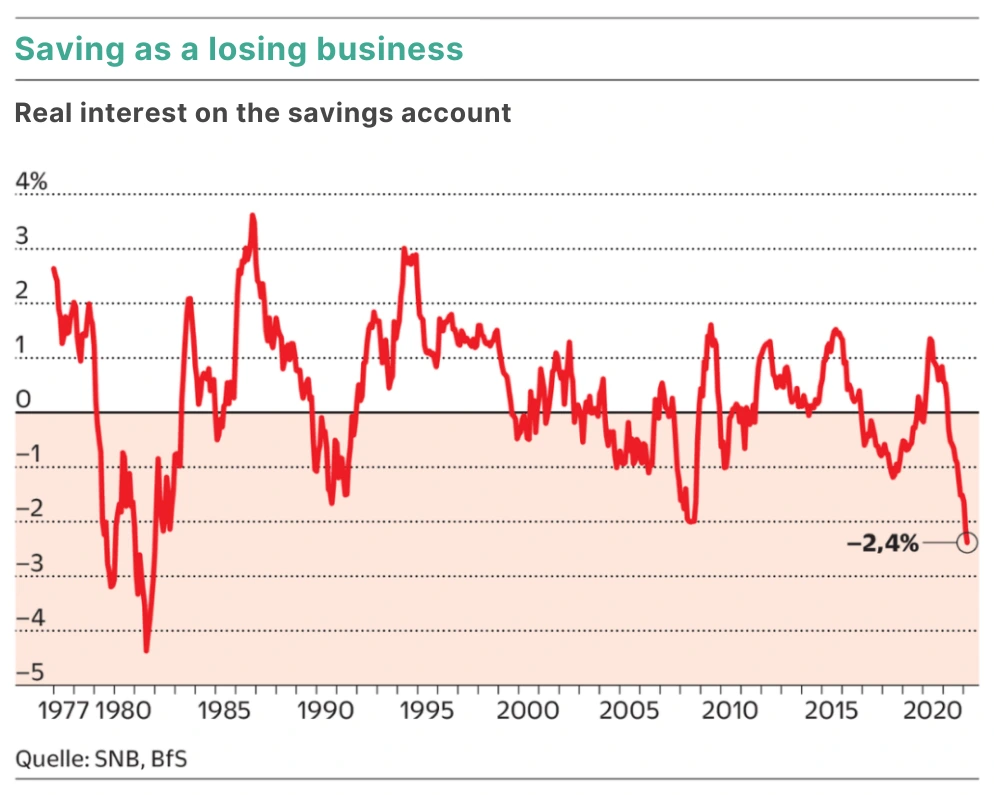

Inflation, and thus the devaluation of money, not only affects the purchasing power, but all assets. As we know, the interest rate on bank accounts has been 0% for many years (not to mention the possible negative interest rates that banks charge the depositors in the worst case scenario). This, together with the inflation in Switzerland, results in a negative real interest rate, which the NZZ am Sonntag recently visualized perfectly. “Saving as a losing proposition” was the headline of the graphic and shows that the real interest rate on savings accounts is as low as it was 40 years ago.

As at summer 2025, the real interest rate is slightly negative (SNB key interest rate is 0% minus inflation of approx. 0.2%).

It is highly unlikely that banks will pay interest rates on savings accounts anytime soon. Therefore, you should act now to combat inflation affecting your savings.

Investment app instead of savings account

Despite inflation, you should of course always have a liquidity cushion in the form of savings. Depending on your circumstances and the scale of your short and medium-term plans, this cushion should amount to a few months’ salary. Savings accounts have definitely outlived their usefulness as an actual investment instrument/savings instrument. To ensure that you still benefit from the compound interest effect, you can invest your savings on the financial market. With the findependent investment app, you can easily benefit from the long-term growth prospects of the financial markets.

You don’t need any previous experience. You can start with as little as 500 francs. After that, you can make deposits of any amount. But first we’ll show you everything you need to pay attention to when investing:

These are the three factors you should pay attention to

1) Diversification

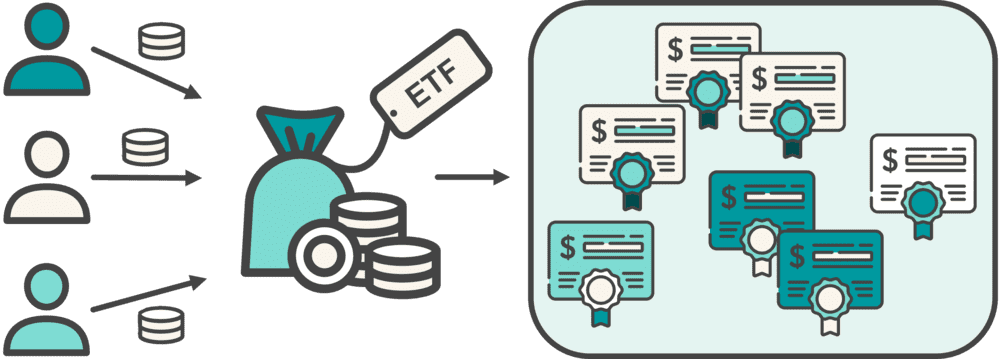

Even if there are major concerns about inflation in Switzerland: Buying individual shares is definitely not a good way to start investing. You may like brands such as Apple, Tesla, Logitech or BMW, but for risk considerations you should always invest broadly. By broad or diversified, we mean investing in a whole range of shares rather than just a few. An ETF, an exchange-traded fund, is best suited for this. It tracks the respective stock market index and allows you to participate in the performance of the overall market easily and cost-effectively.

How an ETF works

An ETF is an exchange-traded fund that tracks an index, for example the Swiss Performance Index (SPI).

Many different companies are represented in an index; in the example of the SPI, almost all Swiss stock corporations listed on the stock exchange are represented.

This means that your money is diversified when you buy an ETF. Diversification is one of the most important principles when investing. It protects you from unnecessary risks. If you were to buy a single share and that company went bankrupt, you would lose all your invested capital. It can be ruled out with a probability bordering on certainty that all the companies in an index will go bankrupt, rendering the ETF worthless.

For income in the form of dividends (for equities) and interest income (for bonds), there are two options: Distribution or reinvestment.

Instead of the income being transferred to your account, it remains invested in the ETF.

- Distributing ETFs pay out interest and dividends

- Accumulating ETFs reinvest the income

2) Investment horizon

Think carefully about how long you can do without the money you are about to invest. If you plan to use the money to buy a house or go on vacation in the next two years, you should not invest it in shares but add it to your liquidity cushion described above.

Money that you are not planning on using for the next 5 years or more can be invested in a findependent investment solution to combat inflation. We explain how this works in detail here.

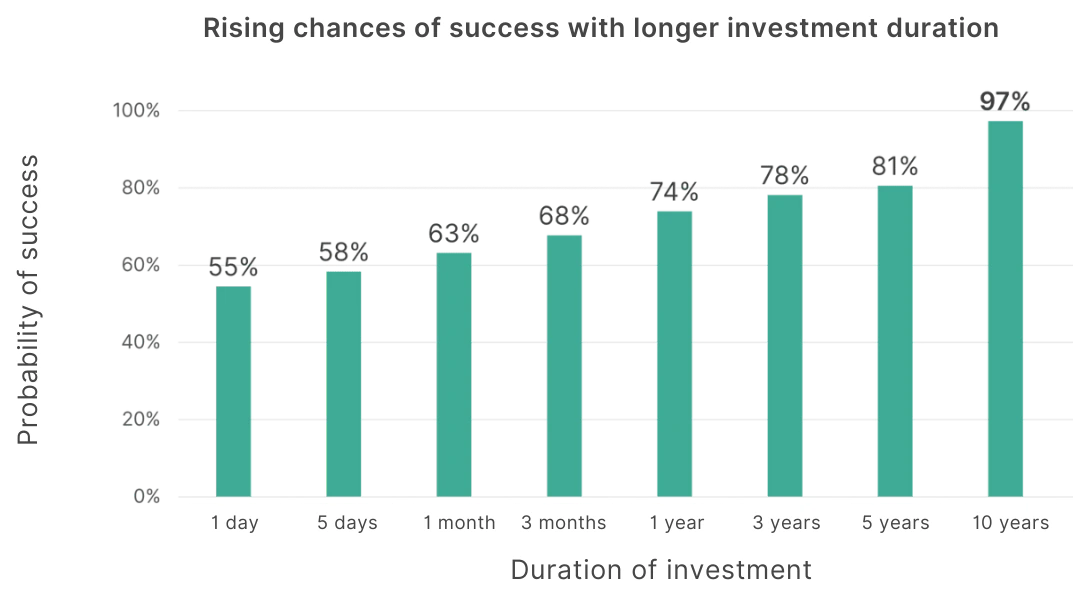

It is particularly important that you let your money work for you in the long run so that you can balance out fluctuations. The longer your money is invested, the greater the probability that you will not realize any loss, or in other words: the smaller the risk. This bar chart visualizes this impressively. With an investment period of 10 years, the probability is already 97%.

The figures in the chart are based on any investment date in the last 30 years.

3) Fees

People often pay little to no attention to the costs of financial products. This probably has something to do with the fact that a fee of 1.something% is seen as a rather small figure. Over time, however, this accumulates to a substantial difference in returns. However, it is also clear that not everything can be free.

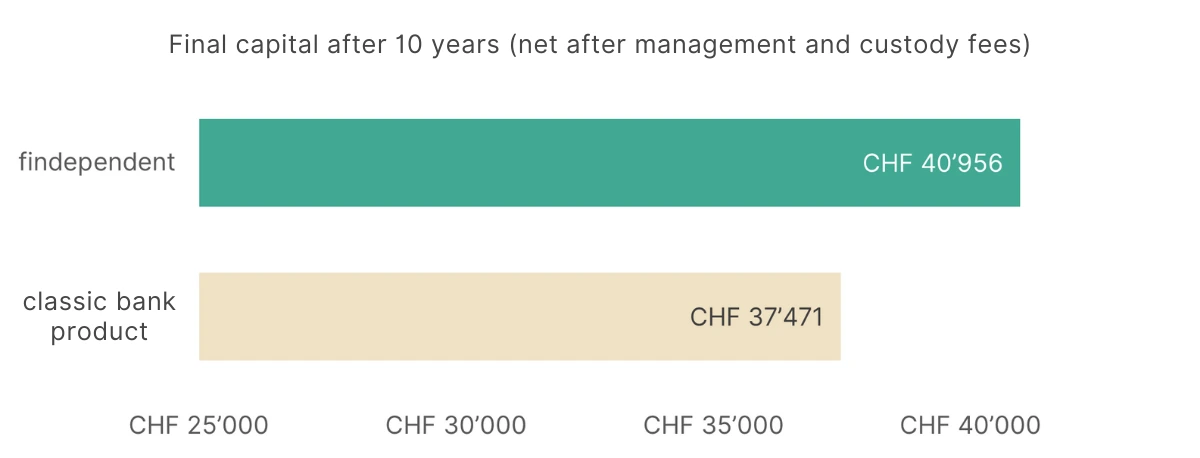

Therefore, we have put together an example of a calculation that compares the fees charged by findependent with the usual costs at banks and shows the effects on long-term asset growth.

Fee comparison:

| classic bank product | findependent investment app | |

| Annual management & custody fee in percent | 1.37% | 0.44% |

| Annual management & custody fee in CHF (for an investment amount of CHF 25,000) | CHF 342.50 | CHF 101.20 |

Note: With findependent, you invest the first CHF 2,000 free of charge.

The figures for the classic bank product are based on a broad-based analysis by the online comparison portal Moneyland from fall 2021.

With an investment sum of CHF 25,000 over an investment horizon of 10 years, the return advantage of the findependent investment solution accumulates to CHF 3,485.

If you want to calculate the benefits of a findependent investment solutions yourself and see how you can counter inflation, use our compound interest calculator:

Assessing the risks

Nothing happens without risk, but without risk nothing happens. Beim Anlegen -um den Einfluss der Inflation auf dein Erspartes einzudämmen- ist äusserst wichtig, dass du dir deiner Sache sicher bist und nur Anlagen tätigst, mit denen du nachts auch noch gut schlafen kannst. Bedenke aber auch, dass das Bunkern von Geld auf dem Sparkonto und die damit einhergehende Geldentwertung ebenfalls ein Risiko darstellt.

When investing – in order to limit the impact of inflation on your savings – it is extremely important that you are sure of yourself and only make investments that you can sleep well with at night. But also bear in mind that stashing money in your savings account and the associated devaluation also represent a risk.

Here a quote from André Kostolany, a luminary in the investment business: “Buy shares, take sleeping pills and stop looking at them. After many years you will see: You are rich.”

Shares as protection against inflation?

In times of inflation, shares can be a good protection against the devaluation of your savings. This is especially true if inflation rates are no higher than 5% per year according to a study from August 2021. Inflation in limited quantities gives companies the opportunity to adjust the prices of their products and services. On the other hand, inflation reduces companies’ debts.

DThe study also concludes that international diversification is an important aspect. “US equities, for instance, achieve +6% and +9% real annualized return in UK and Japan inflation periods”, the authors write.

However, equities do not offer perfect protection against inflation. Nevertheless, you can counteract the devaluation of your savings in your savings account.

Is now the right time to invest?

Geopolitical uncertainties are omnipresent and once a crisis has (seemingly) been overcome, the next challenge arrives. None of us are fortune tellers and gazing into a crystal ball rarely brings the desired enlightenment. Predicting the level of inflation in Switzerland and developments on the financial markets with absolute certainty is simply impossible. We don’t pretend that we can. Instead, we are guided by the insights gained from long-term data.

If you invest regularly (instead of all at once), you benefit from a smoothing effect, also known as the cost averaging effect. For example, if you pay CHF 5,000 into your findependent account every quarter, you buy fewer shares when prices are high and more shares when prices are low. This smooths out the average purchase price. We explain this in more detail in this blog post.

For the sake of completeness, we would like to mention here that there are also empirical studies that show that it is always better to pay in the full amount immediately. We believe this too. However, it is important to note that these studies assume that you as an investor will always keep yourself composed, even if a temporary market drop causes an unrealized loss of any amount (i.e. -40% or more) in the week following your investment.

If you have strong nerves, you can deposit everything at once. If you prefer the option that is easier on your nerves, you should invest in regular steps over a limited time horizon, not over several years.

Conclusion

- Holding excessive account balances is no longer an option due to inflation and currency devaluation

- Invest your medium and long-term available assets

- Pay attention to diversification, investment horizon and fees

- Choose a simple, transparent and inexpensive solution, no complicated things

- Don’t put it off, start today

This might also interest you

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent