The gender investment gap

What findependent does about it and what you should consider as a woman when investing

Globally, men hold more wealth than women. There are various reasons for this, one of which is that women invest less money than men. We’ll explain the facts and show you what you should consider as a woman when investing. We’ll also give you an insight into findependent and how we aim to make investing accessible to everyone.

The Gender Investment Gap

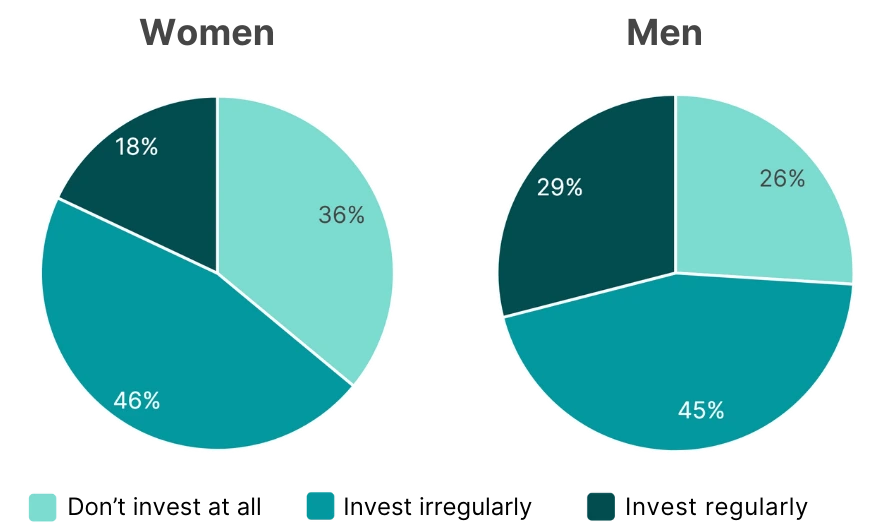

Only 18% of women invest regularly. This is according to a recent study by J.P. Morgan, which surveyed women aged 30 to 60 across 10 different European countries. The study also reveals that over a third of women do not invest at all, compared to about a quarter of men. Additionally, women invest a smaller portion of their savings compared to men.

The size of the investment gap between genders, known as the «Gender Investment Gap» is highlighted by the following finding: If women invested at the same rate as men, there would be at least $3.22 trillion more in invested personal wealth today. This is the result of a 2021 study by BNY Mellon conducted across 16 markets. Even when looking only at the Swiss market, women could have invested an additional $312 billion—provided they were better integrated into the financial market. (NZZ)

The Most Common Barriers Women Face When Investing

In a study by Fidelity Investments, only 9% of women said they thought they were better at investing than men.

The problem is not only that women feel they aren’t adequately targeted by the male-dominated financial industry, but also a lack of self-confidence. In a study by Fidelity Investments, only 9% of women said they thought they were better at investing than men.

Other hurdles: Women tend to believe that they earn too little to be able to invest. In addition, many women consider investing in shares to be too risky for them. (BYN Mellon)

Women are the better investors

Although, as mentioned, very few women think of themselves as such, there is growing evidence that women actually invest more successfully on average than men. For example, another study by Fidelity Investments shows that women achieved an average return of 0.4% more than their male counterparts over a period of 10 years. At first glance, this doesn’t look like much, but due to the compound interest effect, the 0.4% makes a big difference, especially in the long term.

So why is it that women are better investors? They tend to avoid one of the most common investment mistakes: being too active. Women tend to be more patient and long-term oriented and invest diversified. Men, on the other hand, act more impulsively and buy and sell more quickly. In addition, women research more carefully and weigh up the risks better before buying.

This shows: Even if investing is perhaps still a little foreign to you, you can still believe in yourself and dare to tackle the topic, because as a woman you are just as capable of investing successfully!

Especially if you are affected by pension gaps – as many women unfortunately are – you should definitely consider investing.

〉 In this blog post, you can find out how pension gaps occur and other tips on how you can avoid or close them.

〉 We also show you other good reasons why you should invest money as a woman in this blog post.

Investing as a woman

At findependent, we believe that women, like men, should have the confidence and ability to invest in the same way, without needing special products. However, investment solutions should still be tailored to individual needs and personal situations. This approach applies to everyone, regardless of gender.

As a young woman earning a full salary, you can tend to take more risk and invest most of your money in shares, or choose an investment solution that has a higher proportion of shares. If you later start a family, reduce your workload and your income decreases, it is advisable to reduce the risk and invest more in bonds instead of equities, for example.

The risk you want to take can be further influenced by investing a greater or lesser proportion of your savings. As a rule of thumb, you should always leave at least 3-6 months’ wages in your savings account as a “nest egg”. If you have a family and share the financial responsibility of children, it is advisable to increase this reserve of liquid assets.

It is also important that you consider the extent of temporary losses you can personally withstand when investing. This is because the value of your investment solution will fluctuate over the years – to varying degrees depending on the proportion of shares in the investment solution – and temporary losses of 30% to even 50% are quite possible in extreme situations. Under no circumstances do you want to sell your investments at rock-bottom prices in times of crisis because you can no longer bear the loss.

How to find the right investment solution with findependent

findependent offers five ready-made investment solutions, each with a different allocation between the asset classes equities, bonds and real estate:

Careful (20% equities) | Cautious (40% equities) | Balanced (60% equities) | Brave (80% equities) | Risky (98% equities)

When you open an account, we use a questionnaire to determine your investment profile tailored to you and your life situation, on the basis of which we suggest one of these five investment solutions. You can accept our proposal or choose one of the other investment solutions.

You can then change your investment solution at any time without incurring any extra fees. You can either fill out the questionnaire again and ask for our recommendation again or change your investment solution directly in the app.

Investing with findependent

With findependent, we have set ourselves the goal of making investing and the associated financial benefits accessible to everyone.

With us, you don’t need to have a lot of prior knowledge or already own a fortune to get started. Whether it’s opening a digital account, a clear selection of investment solutions or straightforward management in the user-friendly findependent app – we make investing as easy as possible for you, without any technical terms and understandable even for financial newbies.

With findependent, you don’t have to constantly deal with the financial markets and study any annual reports or quarterly figures, but simply invest with a very broad base. You benefit from the current income and the long-term increase in the value of your investments.

You can start with as little as CHF 500 and then flexibly invest more if you wish. You’ll see: even small amounts make a big difference over time! You can find a few calculation examples in this blog post.

We select our investments independently and only in your interests. We keep costs low and only use foreign investments that exclude controversial industries and products such as coal mining, nuclear power, controversial weapons or tobacco.

Conclusion

Unfortunately, women are still lagging behind men when it comes to investing. However, they do not need to invest any differently than men. In order for more women to gain access to investing, it is up to them to take more control of their own financial education and planning. On the other hand, the players in the financial industry must show more effort to better integrate women.

At findependent, we are committed to providing access to investing for everyone. We want to enable everyone to make more out of their own savings and thus live a more financially independent and self-determined life – financially independent or findependent for short.

This might also interest you

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent