Passive or active investing?

Comparison and difference – simply explained

An asset manager can manage the entrusted funds either passively or actively according to the investment style. The same applies to investment funds, where there is also active and passive management. We explain what this means, how the investment styles differ and where the respective advantages and disadvantages lie.

Let’s start with an overview that shows the differences at a glance.

Investment style active vs. passive -differences

| Investment style active | Investment style passive | |

| Allocation / choice of investments | Asset manager makes individual investments decisions | Asset manager follows the index |

| Goal | Outperformance compared to the index | Return close to the index |

| Costs | Expensive | low cost |

| Team | Large number of economists, financial analysts and portfolio managers | Small team, lean organisation |

| Processes | Loads of manuel processes and decisions | High degree of automation |

What is an index?

An index is a kind of basket with a large number of securities in it. When we talk about a stock index, this basket contains a large number of stocks i.e. shares. In concrete terms, for example, the Swiss stock index SPI is a basket with almost all exchange-traded Swiss companies, well over 200, from large (Novartis) to small (Titlis Bergbahnen). The SPI therefore represents the Swiss stock market.

Consequently, the same applies to the stock index called “Nikkei” (Japanese stock market) or the Swiss Bond Index (Swiss bond market).

What is the purpose of an index?

Often the index is used as a benchmark for the performance mesaurement of an investment solution. If the portfolio return is below the index return, this is referred to as underperformance. The opposite case is called excess return or outperformance.

Another use of an index is simply replicating the overall market. With a fund that is oriented towards the index, an investor can represent the entire market with just one investment.

Passive investment and market mapping

The passive investment style aims for a return that is very close to the benchmark index. This is sometimes simply called the “market”. No attempt is made to generate an additional return through individual bets. This is not even necessary, because the long-term trend on the financial markets is positive. This means that the passive investment style does not expose itself to the risk of betting on the wrong horse and thus achieving a return that is significantly below the benchmark index. The only difference to the index return is the management fee. We’ll come back on the fee level and its significance later.

Track the market with ETFs

Since investors cannot simply “buy the market”, they need a solution that tracks the desired index. And it needs to be cost-effective. Exchange traded funds (ETFs) do just that. Investors can invest broadly with just one investment. An ETF on the Swiss stock market index, for example, is representative of the entire Swiss stock market. ETFs are convincing because of their low costs and high transparency.

ETFs enjoy great popularity

Passive investing with low-cost ETFs is indeed very popular. This is also reflected in the flow figures that are regularly published by the major data providers. More money is now flowing into passive than active investment styles in Europe, as figures from fund data specialist Accelerando show.

While passive investment styles have seen strong inflows in the last three months, actively managed funds have suffered outflows of investor money.

Source: accelerando associates, June 2023

The trend has been going on for a while. Since the beginning of 2022, inflows of almost 200 billion euros into passive investment styles have been recorded, compared to outflows from active strategies of over 240 billion euros.

Source: accelerando associates, June 2023

Actively seeking outperformance

The goal of an active investment style is to achieve an excess return over the benchmark index. An investment fund with an active investment style aims to beat the market.

This is to be achieved by means of ongoing, active adjustment of the weightings of individual securities or industries and sectors or even entire countries and regions. The determination of these weightings is also called asset allocation. This allocation is often determined by an entire team consisting of economists, analysts and fund managers. They evaluate a variety of data on each investment in the portfolio, from quantitative and qualitative data on individual stocks to broader market trend and economical factors. Based on this information, the team buys and sells securities to take advantage of short-term price fluctuations. For example, They decide whether to buy pharmaceutical stocks rather than technology stocks on a given day, or whether UBS shares should replace those of Nestlé. We will see below how many fund managers are actually successful with this approach.

Passive or active – comparing like with like

Often the return of actively managed funds is compared with the index return. This is not entirely correct. On the one hand, the net return of the active fund includes its management costs. In concrete terms, the management costs (e.g. 1.75%) are deducted from the performance achieved (e.g. +6.50% gross). This leaves a net return of 4.75%. On the other hand, the index itself cannot be “bought” directly, but an instrument, in this case an ETF, is always needed to replicate the index. Actively managed funds should therefore not be compared with the performance of an index, but always with passive alternatives, i.e. ETFs. That is exactly what we do in this comparison.

Investment style active or passive – fee comparison

When it comes to fees, the facts are clear. The passive investment style is significantly cheaper. But why is this the case?

| Investment style active | Investment style passive |

| Specialists and experts do not work for free, of course, and therefore initially incur high costs. The costs are covered by the administrative fee. The fee level is determined individually by the provider. There is no fixed amount, but around 2% and more is a realistic value. Thus, a return which is 2% higher than the benchmark must be achieved. And you are only on a par with the index return. | The passive investment style requires a minimum of human resources. At the same time, safety and risk control are not lost sight of. Here, too, the costs are covered by the administrative fee. A reasonable amount is in the range of half a percent (0.50%) and already includes the custody fee, which is around 0.15-0.30%. The return of a passive investment instrument is therefore always slightly lower than the return of the benchmark index (by the fee level). |

Active investment style – DIY?

To reduce the high costs of active management, you can also do it yourself. In addition to constant portfolio monitoring, a high degree of market analysis and expertise is required to determine the best time to buy or sell. And watch out: Without constant attention, even the most carefully managed portfolio can easily fall victim to volatile market fluctuations and incur short-term losses that can impact long-term returns.

For this reason, active investing is not recommended for most investors, especially when it comes to their long-term retirement savings.

Passive investing made easy

To invest your savings passively, you shall choose a digital asset manager. Ideally, they also offer their services via an investment app. Like findependent. The investment app is not only cheap, but also simple and transparent.

What and who is findependent?

findependent is a startup based in Switzerland. The investment app, developed and maintained by the 8-member team, makes low-cost investing possible for everyone. Without prior knowledge and expertise. Simple and inexpensive.

Active investment style hardly successful in the long term

Achieving a 2% excess return to cover the high management costs is quite a feat. This is only achieved by very few specialists and only with bold bets in the allocation.

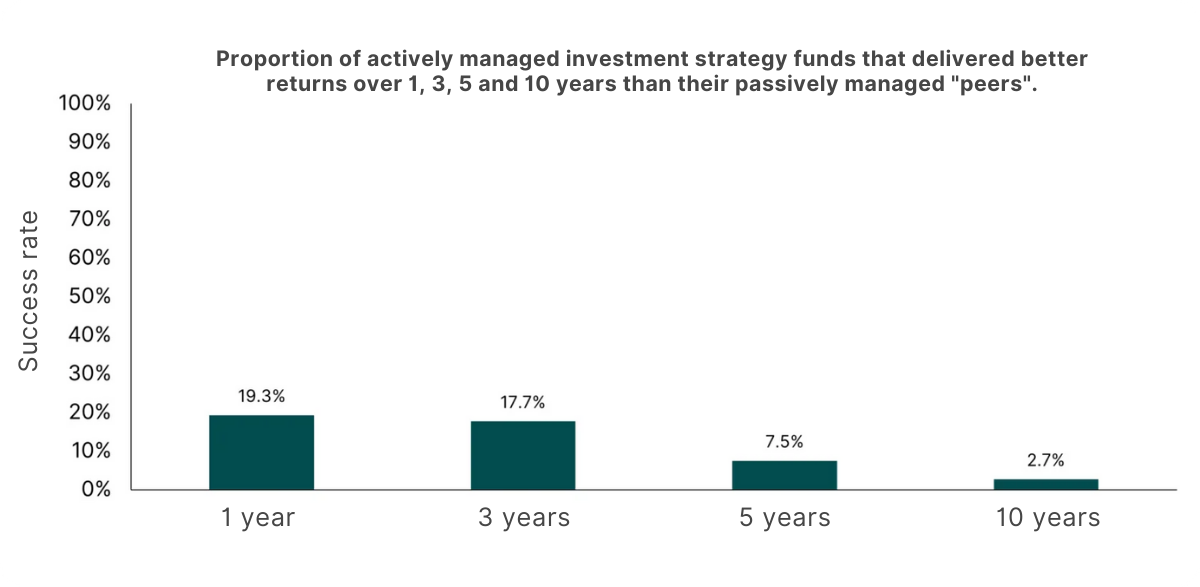

The main problem is that there are hardly any active fund managers who can outperform over a long-term horizon. They lack consistency; one year they are outperforming, the next year underperforming. A study by Morningstar found that among defensive asset allocation funds, over a 10-year horizon, only just 2.7% of actively managed funds were successful. Even when looking at a short-term horizon of 1 or 3 years, only one in five funds is successful. In both cases, success means outperforming the passively managed funds in terms of returns.

The data refer to the Morningstar category “EUR Cautios Allocation – Global” as at 31 December 2021.

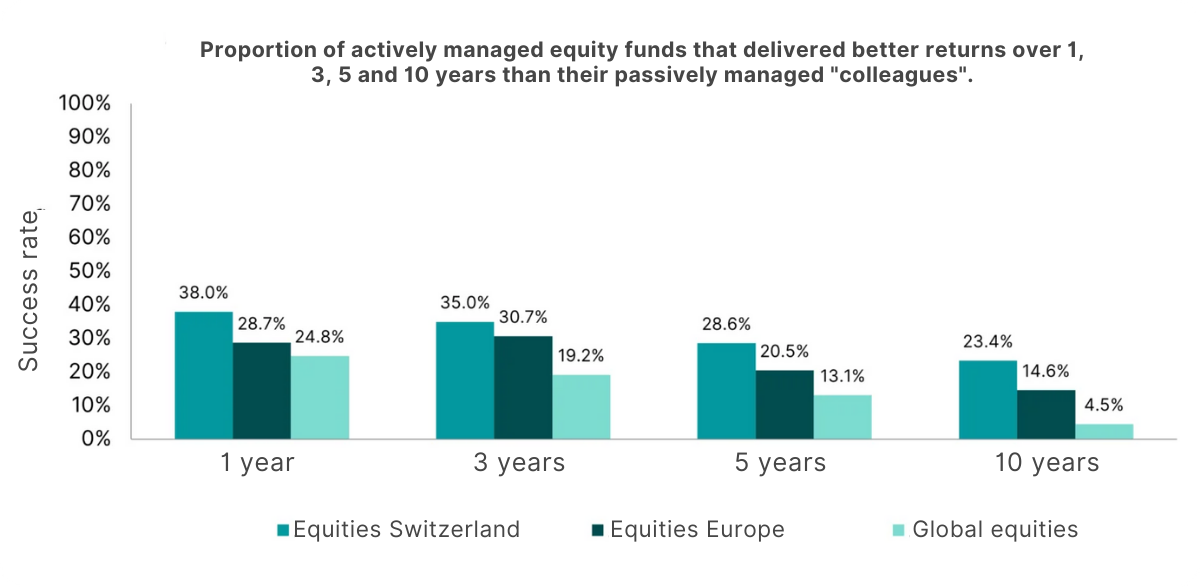

The results for pure equity funds are also rather sobering. In the short term, at least about 30% of the funds can convince, but already after several years the success rate drops and is a meagre 4.5% for global equity funds over 10 years. In other words: 95 out of 100 actively managed funds deliver a return worse than passively managed funds.

The data refer to the Morningstar categories “Switzerland Equity” and “Europe Large-Cap Blend Equity” and “Global Large-Cap Blend Equity”, each as per 31 December 2021.

Morningstar, when asked what investors can learn from this, concludes “…focus on fees… Compared to active funds, passive funds tend to be much cheaper, which makes them hard to beat over the long term.”

Conclusion

- The active investment style tries to outperform the average market return.

- This works out in the fewest cases

- The passive investment style mirrors the average market return.

- Fees are considerably lower with passive investment styles

- Digital asset managers and investment apps make passive investing simple and transparent

You might also be interested in

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://stage.findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://stage.findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent