Pension gaps as a woman

How they arise and how to prevent and close them

On average, women in Switzerland receive 37% less pension than men across the entire pension plan – that is around CHF 20,000 less pension per year or CHF 1,666 per month. As a result, women are twice as likely as men to be affected by poverty in old age after retirement and therefore have to claim supplementary benefits.

In this blog post, we show you how gaps in the 1st and 2nd pillars arise and give you practical tips on how you can avoid and close them.

How and where pension gaps arise

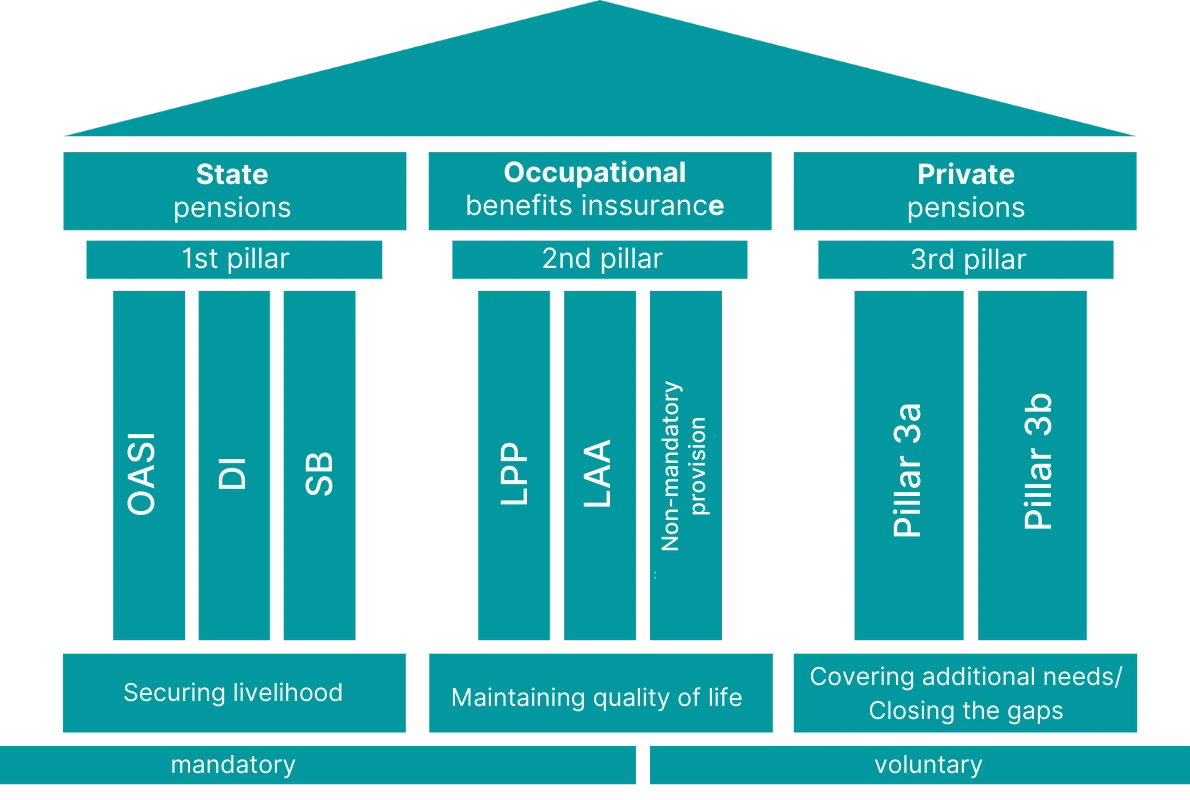

In Switzerland, retirement plans are based on the 3-pillar principle. The benefits of the three pillars complement each other and ensure that you are financially secure after retirement – at least that’s the plan. After all, the pension is not always enough to cover everyday expenses after retirement.

The Swiss pension system

The 1st pillar is supported by the Old-Age and Survivors Insurance (OASI) and the Disability Insurance (DI). Benefits are paid out as pensions and cover (possibly along with Supplementary Benefits (SB)) the basic living expenses.

The 2nd pillar is based on the Occupational Benefit Plan (OP) and the Accident and Occupational Diseases Insurance (UV). Contributions from occupational benefit plans are intended to maintain the standard of living.

In the 3rd pillar, a distinction is made between the tied pillar 3a and the free pillar 3b. It closes existing pension gaps from the other two pillars and covers individual additional needs.

Gaps in the 2nd pillar

Pension gaps for women arise primarily in the 2nd pillar, i.e. the Occupational Benefit Plan (OP). There are many reasons why women tend to be able to pay fewer contributions into the 2nd pillar or are not insured at all.

Lower participation in the workforce

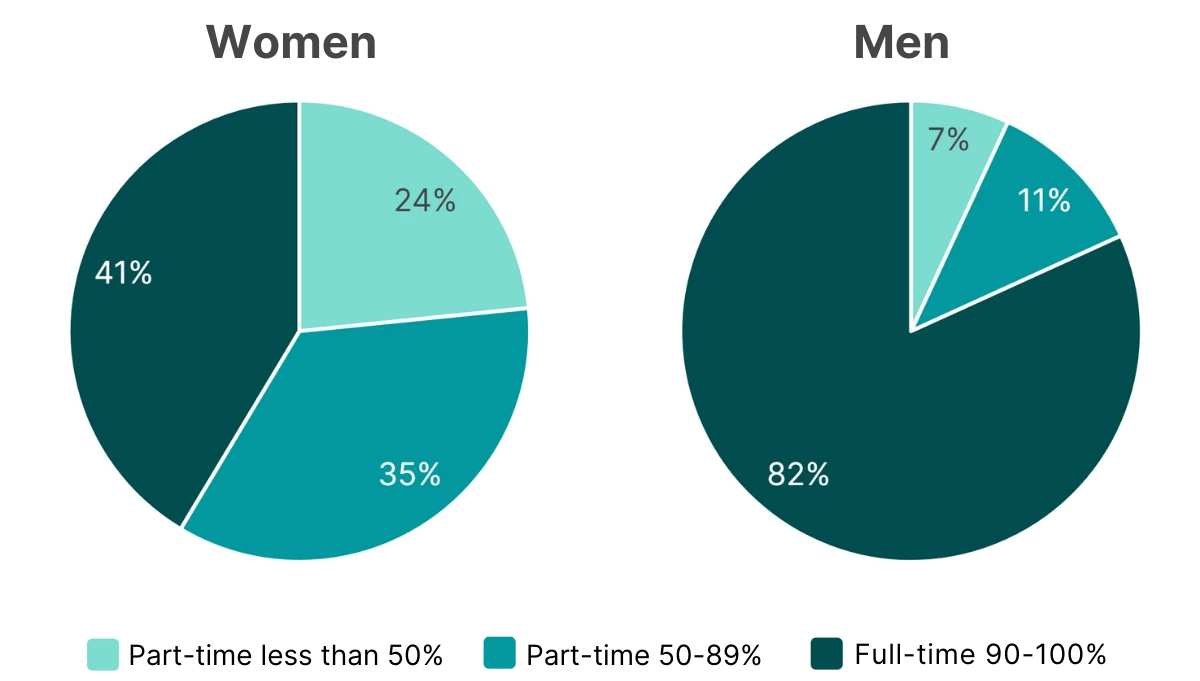

Women perform a large proportion of unpaid household and childcare work, three times more than men worldwide. (UN) At the same time, this means that they have fewer opportunities for paid work. Switzerland is generally a stronghold for part-time work compared to the rest of Europe (NZZ), but the difference between the two genders is very large: while 58.6% of women worked part-time in 2021, only 18.2% of men did so (BfS). A low part-time workload not only means a lower income, but also entails the risk of fewer opportunities for further training and career opportunities.

In addition, women also take longer leaves of absence, particularly due to maternity. Such absences ultimately make it more difficult to re-enter the workforce.

Lower wages

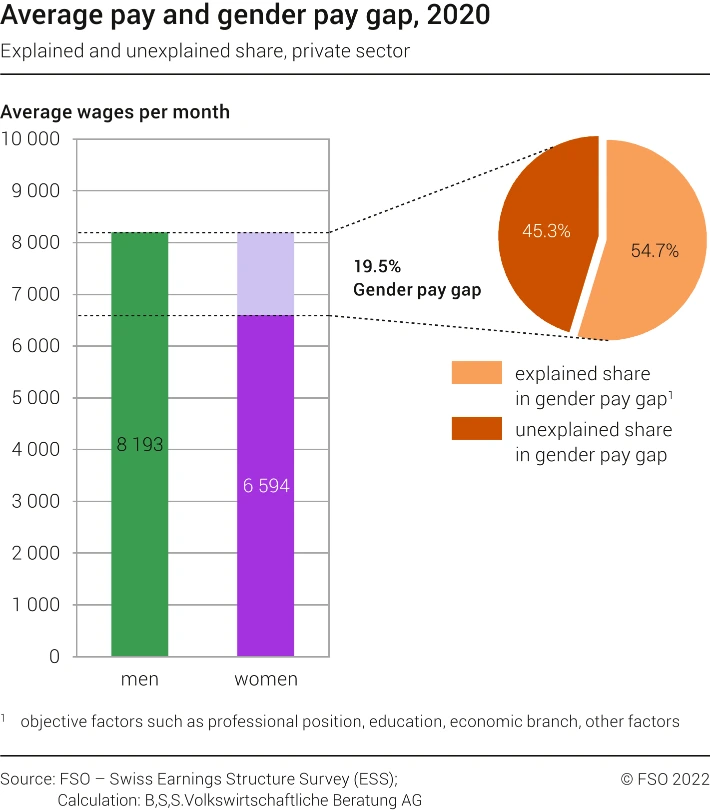

Furthermore, women do not always receive the same salary as men for the same work. Statistics from 2018 show that the wage difference between the two genders in Switzerland was 19.5% on average, but only just over half of this was due to objective factors such as professional position, education or industry. In other words, in the rest of the cases the wage difference was unexplained. (BfS)

As far as the industry is concerned, women are increasingly working in lower-paid professions than men. This particularly affects those who work in so-called “female professions”, where many more women work compared to men, i.e. mainly in nursing, childcare and education. However, the fact that women are more likely to choose to work in these professions or sectors is not due to physical or genetic differences, but rather to social role models and stereotypes that are already evident in children’s books. In addition, adolescent girls in particular take into account criteria such as the compatibility of work and family in the career choice process by choosing a “typical female” profession in advance. (Avenir Suisse)

Entry threshold + coordination deduction

In addition, certain structural conditions of the 2nd pillar put part-time employees at a disadvantage, which again mainly affects women.

Firstly, there is the relatively high entry threshold: a minimum income of CHF 22,680 is required to join a pension fund. Part-time workers with small workloads who do not reach this amount are therefore not covered by the 2nd pillar.

Secondly, there is the coordination deduction: the coordination deduction amounts to CHF 26,460 and is simply the part of income that is already insured in the 1st pillar and is deducted from the insured salary in the 2nd pillar. The purpose of this is to avoid paying social security contributions twice and thus avoiding double insurance. However, the coordination deduction has a disproportionately high impact on part-time workers, resulting in underinsurance in the 2nd pillar for those affected.

Facts about the 2nd pillar

All employed persons are insured in the pension fund (PF), provided they have a minimum income of CHF 22,680 (CHF 1,890 per month).

In the 2nd pillar, you save your own retirement capital and are also insured against certain risks, such as death and disability due to illness or accident. The amount of benefits in the event of an incident (old age, death, disability) depends on your insured salary and your employer’s individual pension fund plan. The employer pays at least half of the contributions.

Social security contributions are calculated on the basis of your insured salary and are deducted from your salary each month. The social security contributions consist of two parts:

- Your savings contributions (retirement credits), which earn interest from your pension fund and add up over the years as your retirement assets, that you eventually receive from the pension fund. Your retirement assets are converted into your pension, which you receive for the rest of your life, based on the conversion rate. For example, if you have saved up retirement assets of CHF 1 million at the current statutory minimum conversion rate of 6.8%, you will receive a retirement pension of CHF 68,000 per year.

- The insurance premiums (insurance cover) for risk protection, i.e. money that you or your family receive in the event of death or disability due to illness or accident.

Retirement assets accumulated during marriage belong to both spouses in equal shares.

Gaps in the 1st pillar

Gaps are also possible in the 1st pillar. They occur when contribution years are missing, e.g. if you are not employed for a year. Common reasons for this are:

- Study

- Traveling / time abroad

- Many and short work assignments with different employers

- Divorce for non-employed individuals if they subsequently forget to pay the minimum OASI contribution

If you are married, gaps are generally not a problem. If, for example, you are not employed during your maternity leave or afterwards with young children, you are covered by your spouse – as long as he/she pays in double the minimum amount.

If necessary, you can fill any gaps with so-called “youth years”. These are contribution years that you have if you were already employed between the ages of 18 and 20.

As a result of contribution gaps, your pension will be reduced. This is referred to as a partial pension (instead of a full pension). If, for example, you have not made any OASI contributions for a whole year, your pension will be around 2.3% lower.

Since your benefits from the 1st pillar depend not only on whether or not you have made annual contributions, but also on the amount of your contributions, part-time work and the associated reduced income also pose a risk to your pension.

Facts about the 1st pillar

The 1st pillar is organized according to the pay-as-you-go principle, i.e. the economically active generation directly finances the pensioners.

Employed individuals pay 5.3% of their salary, or at least CHF 530, into the OASI/DI scheme. The employer pays the same amount.

Non-employed individuals in a marriage are insured through their spouses, provided they pay double the minimum contribution (2x CHF 530 per year).

The size of the retirement pension that you as an individual will receive from the 1st pillar after you retire depends on two factors:

- The number of years in which you have paid contributions

- Your average annual income (the higher your salary, the higher the contributions you have to pay, the higher your pension).

The retirement pension amounts to a minimum of CHF 1,260 and a maximum of CHF 2,520 per month. To receive the maximum pension, you must earn an average of at least CHF 90,720 per year and, nowadays both as a man and as a woman, have paid in for 44 years.

As a married couple or as a couple in a registered partnership, together you will receive a maximum of 150% of the maximum pension, i.e. a maximum of CHF 3,780.

How you can avoid and close pension gaps

Here’s the good news: you don’t have to accept gaps in your pension fund just like that – there are various things you can do about them! Here are our practical tips.

Dividing employment, household and childcare responsibilities fairly

Based on the results of its study, the Swiss Conference of Gender Equality Delegates recommends that women and men work at least 70% on average throughout their working lives. This way you run the least financial risk, even in the event of divorce.

This means that in a marriage/partnership, work, household chores and childcare should be divided in a way that allows women to work at a higher percentage right from the start.

However, this is not always possible or desired. In such a case, the person earning (more) could also compensate the other person financially for the unpaid household and/or childcare duties, e.g. in the form of contributions to the 3rd pillar.

Either way, it is recommended that you and your partner/(future) spouse consciously address this issue and make agreements – however unromantic it may be. Because it’s about your financial independence!

Examining and filling gaps in the 1st and 2nd pillars

OASI

The “individual account” (IC) forms the basis for calculating your pension and is held by the compensation offices. If you are unsure whether you have OASI gaps, i.e. missing contribution years, you can easily order an extract from your IC free of charge. You can find all the information and a great explanatory video here.

If you have gaps in your OASI, you have the option of paying contributions retroactively for 5 years. It is therefore best to order a statement from your IC every 3-5 years.

Pension fund

If you change your job, you will usually also change your pension fund. The contributions you have made up to that point will then be transferred to your new pension fund. You will be asked to do this in writing by your previous pension fund. However, if you fail to do so, your pension fund assets will become “contactless vested benefits”. You can fill out a form on the website of the LOB Guarantee Fund Foundation to check whether a vested benefits account with pension assets has been set up for you.

It is best to regularly order a pension fund statement from your PF to see where you stand with your retirement assets.

If you work part-time, we also recommend that you talk to your employer. Depending on this, they may be willing to adjust the entry threshold and/or the coordination deduction of your pension fund to your workload. And if you have several jobs, it is worth finding out whether your pension funds can be combined.

With some pension funds, it is possible to make additional voluntary contributions (so-called “pension fund purchase”). This would therefore be one way of closing any gaps. However, compared to other pension options, buying into a pension fund is only worthwhile in rare cases. More information in this blog post.

Investing money in the 3rd pillar

In addition to the 1st and 2nd pillars, it is worth voluntarily using the 3rd pillar to provide for your retirement. We explain the differences between the bound pillar 3a and the free pillar 3b in this blog post.

For the 3rd pillar, it is worthwhile not simply leaving your assets/money in a savings account, but investing them in assets such as shares. This way, your savings can generate continuous income and grow until you retire. And because of the compound interest effect, it’s best to start investing money in the 3rd pillar at an early age and not wait until you notice gaps in the 1st and/or 2nd pillar. Incidentally, you can deduct your pillar 3a contributions from your taxable income. For 2026, the maximum contributions have been increased to CHF 7,258 (with a pension fund). For those without a pension fund, the maximum tax deduction is 20% of annual income (less social benefits), or a maximum of CHF 36,288.

〉 In addition to making smart provisions for old age, there are other good reasons why you should invest as a woman. We’ll show you in this blog post.

Investing is not as complicated as many people initially think. If you stick to a few principles, you can significantly reduce the risk and still save cleverly for the future. Above all, it is important to invest as broadly and regularly as possible and to hold your investments for a long time.

〉 In this blog post on the gender investment gap, we explain what else you can consider when investing as a woman.

Conclusion

Unfortunately, pension gaps are a reality for many women and lead to poverty in old age more often than expected. That’s why it’s important that you deal with your pension provision at an early age and know the potential pitfalls. By reading this blog post, you’ve already taken the first step, great! But it certainly wouldn’t hurt to build up further financial knowledge. If your situation is complex or still very unclear, it may be worth seeking individual advice. And it’s always good to talk to other women about such topics!

You might also be interested in

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_partnerangebote_in_der_findependent_app_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:182024-10-16 13:30:34Partner offers in the findependent app https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_wie_du_dein_geld_besser_sparen_kannst_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-11-05 13:08:542024-07-11 14:09:425 tips on how to better save your money https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund?

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_saeule-3a_freies_vermoegen_oder_pensionskasse_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:43:312026-01-26 16:57:02Pillar 3a, free assets or pension fund? https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman

https://stage.findependent.ch/wp-content/uploads/2023/09/findependent_vorsorgeluecken_als_frau_blog_banner.png

444

668

findependent-admin

https://stage.findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:422026-01-29 16:51:51Pension gaps as a woman